PPh Orang Pribadi (Update 2023) - 6. PPh Pasal 24 (Kredit Pajak Luar Negeri)

Summary

TLDRIn this video, the presenter explains the concept of Article 24 of the Indonesian Tax Law, which involves foreign tax credits. The video details how to calculate the tax that can be credited from foreign sources by comparing the actual tax paid abroad to the calculated tax in Indonesia. Using examples from the U.S. and Singapore, the presenter walks through the calculations to show how much tax can be credited. The video provides an easy-to-follow breakdown of how foreign taxes work in relation to Indonesia's tax system, aiming to simplify complex tax matters for viewers.

Takeaways

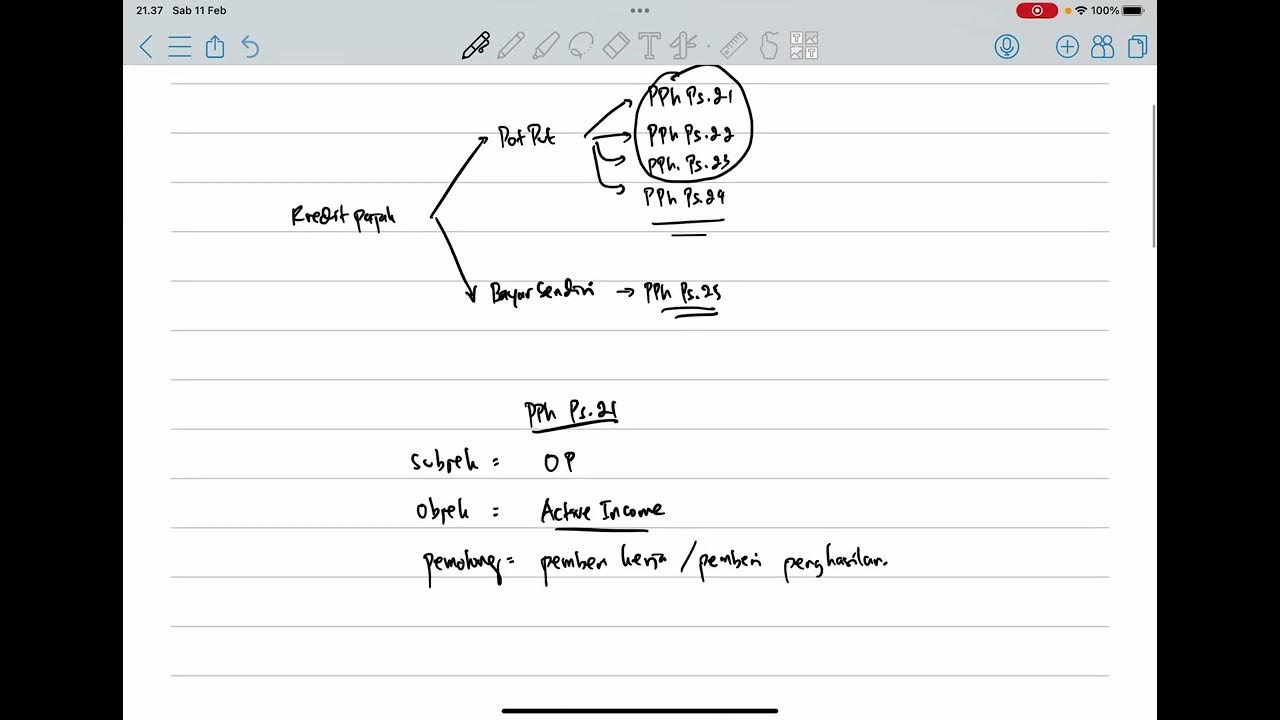

- 😀 PPh Pasal 24 refers to the Foreign Tax Credit in Indonesia, allowing taxpayers to credit taxes paid abroad against their Indonesian tax liability.

- 😀 Foreign taxes paid on income abroad may not always be fully credited; the smaller value between the actual foreign tax and the Indonesian tax calculation is credited.

- 😀 To calculate the foreign tax credit, you must compare the actual tax paid abroad and the calculated Indonesian tax based on your total taxable income.

- 😀 If the foreign tax paid is smaller than the Indonesian tax calculated, the foreign tax credit will be limited to the Indonesian tax calculation.

- 😀 The example in the script compares income and taxes from both the United States and Singapore to demonstrate how the foreign tax credit works.

- 😀 Domestic income in the example is 300 million, US income is 100 million, and Singapore income is 200 million, totalling 600 million in income.

- 😀 The tax calculation involves applying progressive tax rates (5%, 15%, 25%, 30%) on the taxable income to determine the total tax due.

- 😀 For the US income, the foreign tax credit calculation results in 19,743,589 being creditable, which is smaller than the 30 million tax withheld in the US.

- 😀 For the Singapore income, the foreign tax credit calculation results in 39,487,180 being creditable, but only the 10 million tax withheld in Singapore can be credited, as it's smaller.

- 😀 Understanding how foreign tax credits work ensures that you don't pay double taxation on income earned abroad, as you can credit the tax paid abroad to your Indonesian tax liability.

Q & A

What is PPh Pasal 24 in Indonesia?

-PPh Pasal 24 refers to the tax credit for foreign taxes paid, allowing Indonesian taxpayers to offset the tax they've already paid overseas against their tax liability in Indonesia.

How is the tax credit for foreign taxes calculated under PPh Pasal 24?

-The tax credit is calculated by comparing two values: the actual foreign tax paid and the tax calculated based on Indonesian income tax rates. The lower of the two values is used as the credit.

What factors determine the amount of the foreign tax credit that can be claimed?

-The amount of the foreign tax credit depends on the actual tax paid overseas and the calculated tax liability based on the taxpayer's total income and the Indonesian tax rates.

Can all foreign taxes be credited under PPh Pasal 24?

-No, not all foreign taxes can be credited. Only the lesser of the actual foreign tax paid or the tax calculated under Indonesian tax rules can be credited.

How do you determine which foreign income qualifies for the tax credit?

-Foreign income qualifies for the tax credit if it is reported as part of the total taxable income in Indonesia and if it has foreign taxes deducted or withheld.

What happens if the foreign tax paid is higher than the tax calculated in Indonesia?

-If the foreign tax paid is higher than the tax calculated in Indonesia, the taxpayer can only claim the Indonesian tax liability as a credit. The excess foreign tax paid cannot be refunded or carried forward.

Can you give an example of how the foreign tax credit works with income from the USA?

-In the example given, if a taxpayer receives income from the USA and foreign tax of 30 million IDR is paid, the credit would be the lesser of 30 million IDR or the tax calculated in Indonesia based on the taxpayer's total income.

What is the method for calculating the Indonesian tax liability for foreign income?

-To calculate the Indonesian tax liability for foreign income, the total income (domestic and foreign) is first determined. Then, the applicable tax rates are applied to this total to compute the tax due.

How is the tax credit for income from Singapore determined?

-For income from Singapore, the foreign tax credit is calculated based on the formula: (foreign income / total taxable income) × Indonesian tax due. If the foreign tax is lower than the calculated amount, the lower value is credited.

Why might the tax credit for Singaporean income be lower than the foreign tax paid?

-The tax credit for Singaporean income may be lower if the foreign tax paid is smaller than the tax liability calculated in Indonesia. In the example, the foreign tax paid was 10 million IDR, which was less than the calculated tax due from the Singaporean income.

Outlines

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantMindmap

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantKeywords

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantHighlights

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantTranscripts

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantVoir Plus de Vidéos Connexes

PPh Pasal 24: Pengertian, Subjek dan Objek, Cara Pelaksanaan Kredit, dan Studi Kasus

Pasal 36 Ayat 1 UU KUP | KEMENKEU GABISA JAWAB PASAL INI MENGIKAT SIAPA !?

Pembukuan & Pencatatan | MOOC | Materi Pengantar Perpajakan Seri 8

Pengenalan PPh Pasal 22, tarif PPh Pasal 22, dan Contoh Soal PPh Pasal 22

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

INTRODUÇÃO AO SISTEMA TRIBUTÁRIO NACIONAL | Prof.ª Lílian Souza

5.0 / 5 (0 votes)