Materi ke 1 Akuntansi Perusahaan Jasa (Kelas XI Akuntansi)

Summary

TLDRIn this lesson, the instructor introduces the fundamentals of accounting for service companies, focusing on key concepts such as the definition of service companies, their characteristics (intangibility, inseparability, variability, perishability), and the accounting cycle. Students learn about recording financial transactions in journals and general ledgers, and the importance of balancing debits and credits. Practical examples illustrate how different transactions, such as capital investments and purchases, are recorded in accounting systems. This session provides a solid foundation for vocational high school students studying accounting in service industries.

Takeaways

- 😀 Service companies primarily focus on providing services to the public rather than selling physical goods.

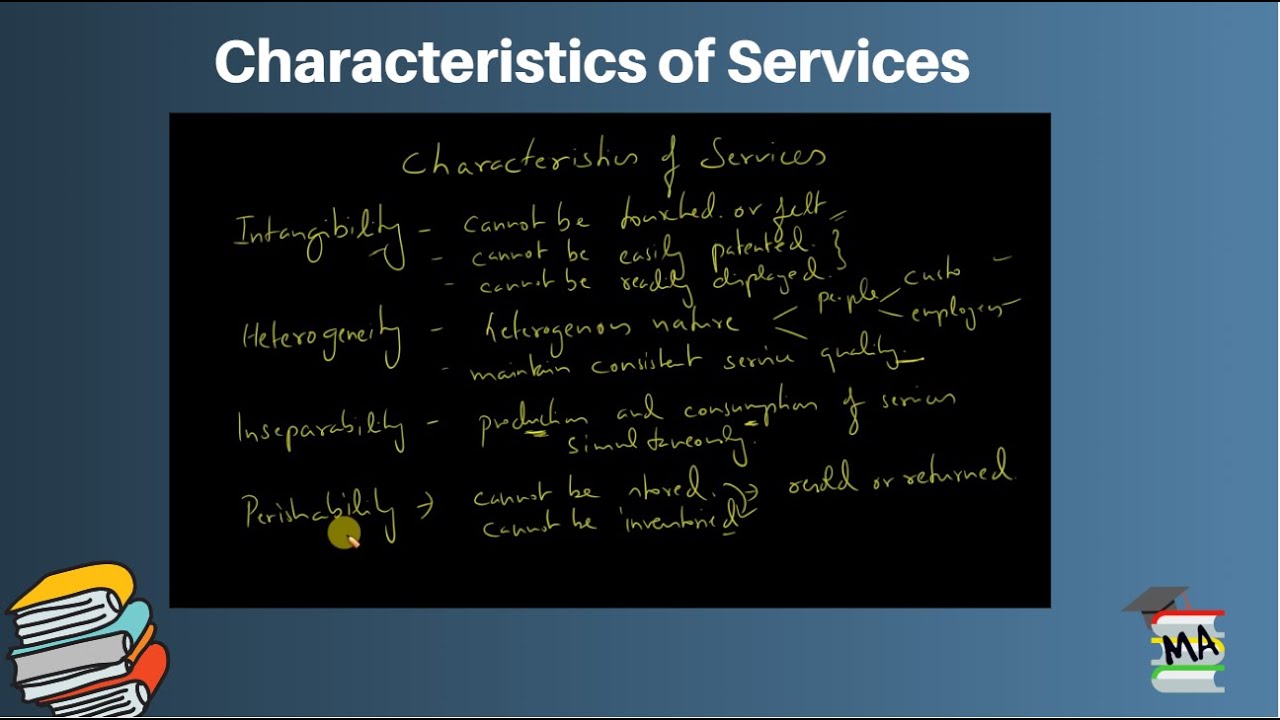

- 😀 The characteristics of service companies include intangibility (services cannot be touched or stored), inseparability (production and consumption happen simultaneously), variability (services are customized based on customer preferences), and non-storability (services cannot be stored or resold).

- 😀 The accounting cycle for service companies includes collecting transaction evidence, recording in journals, posting to ledgers, adjusting for discrepancies, and preparing financial statements like balance sheets and income statements.

- 😀 In the journal entry process, debits are recorded when assets increase or liabilities decrease, while credits are recorded when liabilities increase or assets decrease.

- 😀 An example of a journal entry: When capital is deposited into a bank, the 'Cash' account is debited (asset increase), and the 'Capital' account is credited (equity increase).

- 😀 Journal entries must balance: the total debits must equal the total credits to ensure the accounting equation remains in balance.

- 😀 Service company transactions are recorded chronologically in journals, with clear identification of accounts to be debited and credited.

- 😀 After journal entries, amounts are posted to specific accounts in the general ledger for more detailed tracking of financial activities.

- 😀 The general ledger organizes all transactions by account (e.g., Cash, Capital, Supplies) to keep track of balances and aid in financial reporting.

- 😀 Financial reports, such as balance sheets and income statements, are prepared at the end of the accounting cycle to reflect the company’s financial position and performance.

- 😀 Service companies do not hold inventory like trading or manufacturing companies, as they provide intangible services instead of physical goods.

Q & A

What is the main focus of the subject being taught in this lecture?

-The main focus of the lecture is on 'Accounting for Service, Trade, and Manufacturing Companies,' particularly aimed at class 11 students at SMK Sumatra 40.

What distinguishes a service company from other types of businesses?

-A service company primarily provides services rather than physical goods. The primary goal of a service company is to generate profit by offering these intangible services to the public.

Can you give an example of a service company mentioned in the transcript?

-An example of a service company provided in the transcript is a courier service that delivers goods to customers.

What are the four characteristics of service companies mentioned in the transcript?

-The four characteristics of service companies are: 1) Intangibility (services cannot be physically touched or seen), 2) Inseparability (production and sale happen simultaneously), 3) Variability (service quality varies based on factors like time and customer preferences), and 4) Perishability (services cannot be stored for later use).

How does the accounting cycle for service companies differ from other companies?

-The accounting cycle for service companies is largely the same as for other companies. It includes collecting evidence of transactions, recording them in journals, posting to the ledger, preparing a trial balance, making adjustments, and preparing financial statements.

What is the purpose of the journal in accounting, as explained in the lecture?

-The journal in accounting serves as a chronological record of all financial transactions, showing which accounts are debited and credited. It ensures that every transaction is properly recorded.

What is the difference between a debit and a credit in journal entries?

-A debit increases assets and decreases liabilities or equity, while a credit increases liabilities or equity and decreases assets.

Why is the balance between debits and credits important in accounting?

-The balance between debits and credits is crucial because it ensures that the financial records are accurate. If debits and credits do not balance, it indicates an error in the accounting process.

What happens after transactions are recorded in the journal?

-After transactions are recorded in the journal, they are posted to the ledger, where transactions are grouped by account type, such as cash, supplies, or liabilities.

What is the role of adjusting entries in the accounting cycle?

-Adjusting entries are made to reflect accurate financial data before preparing the financial statements. They ensure that all transactions are accounted for properly and that the company's financial position is accurately represented.

Outlines

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantMindmap

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantKeywords

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantHighlights

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantTranscripts

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantVoir Plus de Vidéos Connexes

Konsep Dasar Pemasaran Jasa

Sistem Layanan Usaha / Materi Produk Kreatif dan Kewirausahaan kelas XI

Konsep Dasar Akuntansi dan Lingkungannya

Service Operations

Characteristics of Services I Intangibility, Inseparability, Heterogeneity, and Perishability

Produk Jasa | Klasifikasi Jasa | Kualitas Jasa | Karakteristik Jasa | Definisi Jasa

5.0 / 5 (0 votes)