Introduction to Accounting for Investments (Equity and Debt Securities)

Summary

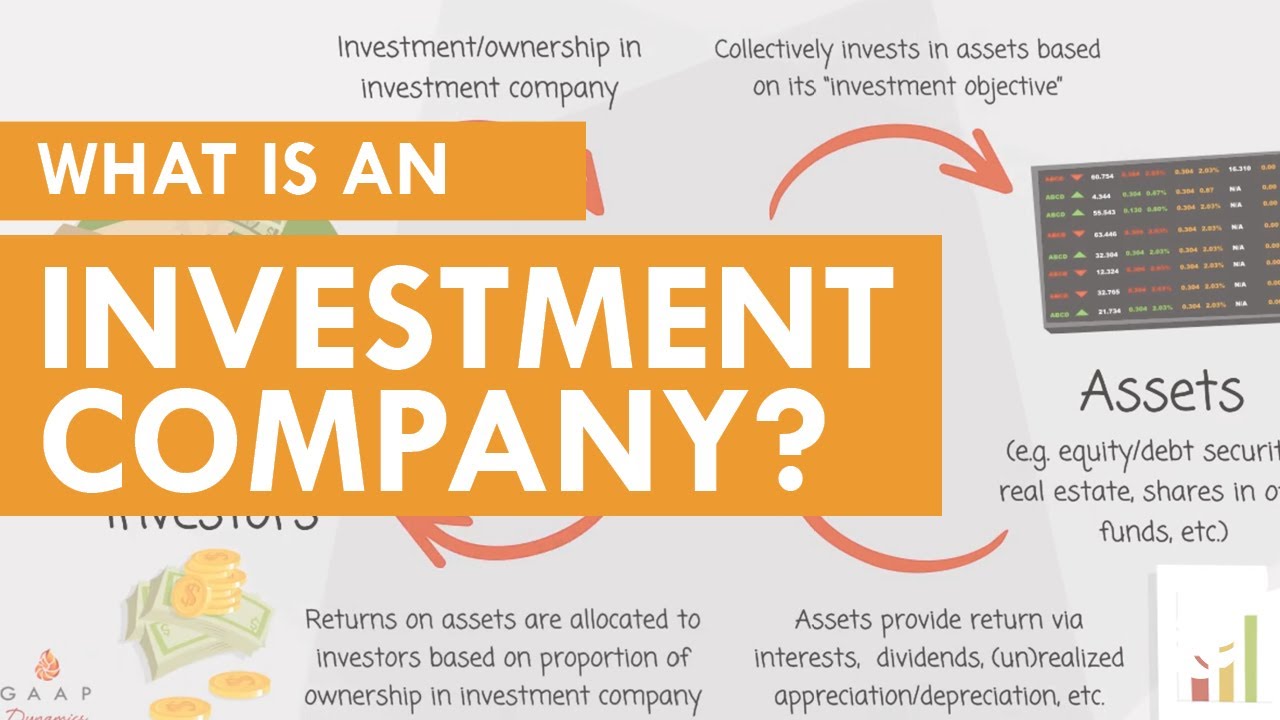

TLDRThis session explores why companies invest in others, such as for diversification or securing operating arrangements. Investments are categorized into debt (like bonds) and equity (like stocks). The accounting treatment varies based on intent and ownership level: held-to-maturity, trading, available-for-sale for bonds; fair value, equity method, or consolidation for equity. The presenter encourages using resources like farhatlectures.com for CPA exam preparation.

Takeaways

- 💼 Companies invest in other companies for various reasons such as entering new markets, diversifying risk, earning a high rate of return, securing operating arrangements, or simply because investing is their core business.

- 🌐 Microsoft's acquisition of LinkedIn is an example of a company investing in another to enter a new market.

- 💹 Diversification of investments is crucial to mitigate risks, especially when the core business might face downturns.

- 💰 Cash is considered the safest investment but offers the lowest return; hence, to earn more, companies invest in other ventures.

- 🔗 Investments can secure critical supply relationships, like electric car manufacturers investing in battery suppliers.

- 🏦 Companies like Berkshire Hathaway exist specifically to invest in other companies, showcasing investment as a standalone business model.

- 📈 Investments are categorized into debt (like bonds) and equity (like stocks), with each requiring different accounting treatments.

- 📉 Debt investments are classified as held-to-maturity, trading, or available-for-sale based on the company's intent.

- 📋 Held-to-maturity bonds are reported at amortized cost, ignoring fair value fluctuations since they are intended to be held until maturity.

- 📊 Trading investments are short-term and reported at fair value, reflecting unrealized gains and losses.

- 📖 The degree of ownership in an equity investment determines the accounting method: fair value for passive investors, equity method for significant influence, and consolidation for control.

- 📚 For a comprehensive understanding of accounting for investments, resources like Farhat Lectures offer additional materials aligned with CPA review courses.

Q & A

Why do companies invest in other companies?

-Companies invest in other companies for various reasons such as investing in startups, entering new markets, diversifying risk, earning a high rate of return, securing operating arrangements, or simply because some companies exist to invest in other companies.

What is the difference between debt and equity investments?

-Debt investments involve lending money to another company, typically by buying bonds. Equity investments involve owning a share of another company, typically by purchasing stocks.

What is the significance of the intent behind an investment?

-The intent behind an investment determines how it is classified and accounted for. For example, if a bond is held to maturity, it is classified as held to maturity and reported at amortized cost.

What does it mean to classify an investment as held to maturity?

-Classifying an investment as held to maturity means the investor has no plan to sell the bond and intends to hold it until it matures, reporting it at amortized cost.

What is amortized cost in the context of bond investments?

-Amortized cost refers to the initial purchase price of a bond, adjusted for any premium or discount, and ignoring fair value fluctuations until maturity.

What are the three categories of debt investments?

-The three categories of debt investments are held to maturity, trading, and available for sale.

What is the difference between trading and available for sale investments?

-Trading investments are intended to be sold in the near future, while available for sale investments fall somewhere in between holding to maturity and trading, where the investor might sell if the price is right.

How does the degree of ownership affect how equity investments are accounted for?

-The degree of ownership determines the level of control or influence the investor has over the investee company, which in turn affects the accounting method used, such as fair value, equity method, or consolidation.

What is the equity method of accounting for equity investments?

-The equity method is used when an investor owns between 20% to 50% of a company, indicating significant influence over the investee, and the investment is accounted for based on the investor's share of the net income or losses of the investee.

What is the consolidation method in accounting for investments?

-The consolidation method is used when an investor owns more than 50% of a company, indicating control, and the investee's financial statements are combined with the investor's.

What additional resources are recommended for understanding accounting for investments?

-The script recommends visiting farhatlectures.com for additional resources, multiple-choice questions, and supplemental materials to enhance understanding of accounting for investments.

Outlines

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantMindmap

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantKeywords

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantHighlights

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantTranscripts

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenant

5.0 / 5 (0 votes)