0902 Componen of Internal Control compressed

Summary

TLDRIn this lecture, Amsal discusses the components of an effective internal control system. He outlines key elements such as the control environment, risk assessment, control activities, and the importance of information and communication systems. Amsal emphasizes the need for robust processes, including task separation, authorization controls, and physical security for assets and records. Regular monitoring of these components is crucial to ensure that internal controls remain effective and aligned with organizational goals. The lecture provides essential insights into how businesses can design and maintain effective internal control systems.

Takeaways

- 😀 **Control Environment**: A strong internal control system starts with a solid control environment, which includes ethical values, integrity, competence, and the leadership's commitment to good governance.

- 😀 **Risk Assessment**: Identifying, estimating, and managing risks are critical. Organizations should assess both the likelihood and impact of risks and take appropriate actions to mitigate them.

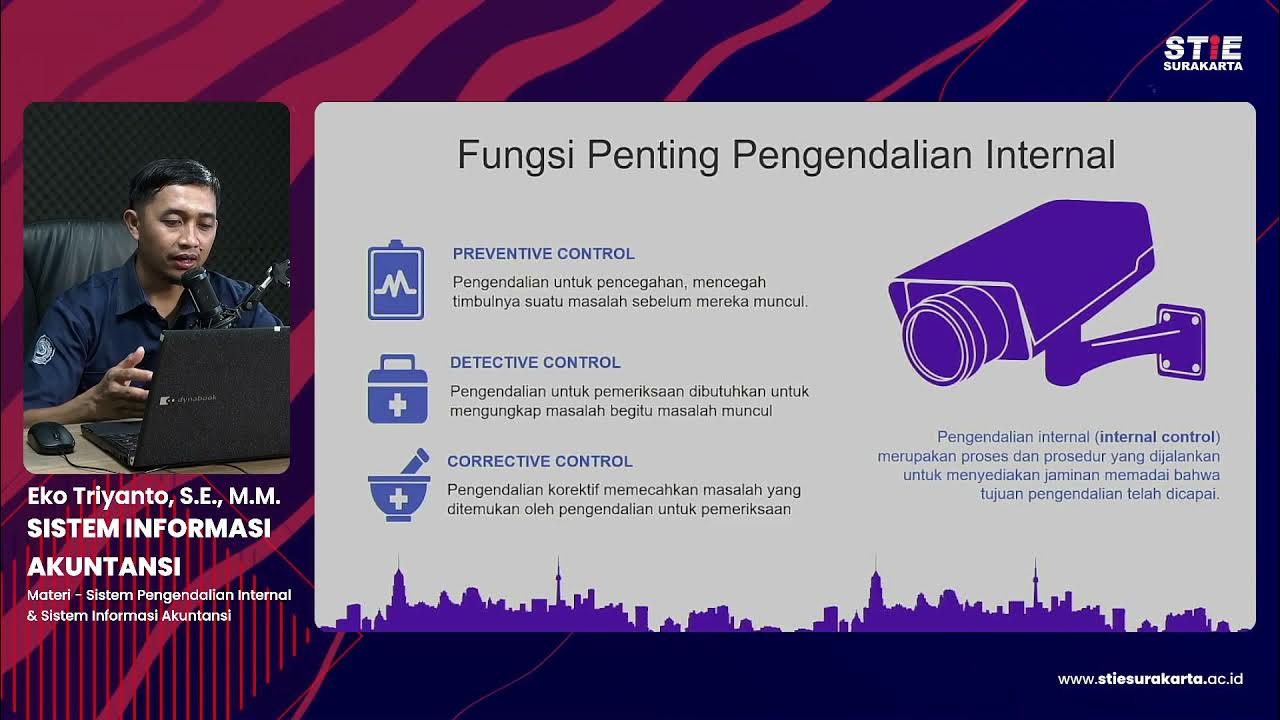

- 😀 **Segregation of Duties**: Ensuring that duties are properly separated, such as separating asset management from accounting, prevents conflicts of interest and reduces the risk of fraud or error.

- 😀 **Authorization of Transactions**: Every transaction must be authorized. There are two types of authorization: general authorization (for general activities) and specific authorization (for specific transactions).

- 😀 **Proper Documentation**: All transactions should be documented properly, including sequential numbering, multi-use formats, and preventative measures to avoid errors or fraud.

- 😀 **Physical Supervision of Assets**: Safeguarding physical assets is essential, such as storing them securely and implementing access controls to prevent theft or loss.

- 😀 **Independent Checks**: Regular independent checks are necessary to ensure that control procedures are being followed and to identify any discrepancies or issues.

- 😀 **Information and Communication Systems**: These systems must be robust and reliable to ensure that transactions are executed properly and that the necessary information is communicated effectively within the organization.

- 😀 **Continuous Monitoring**: The internal control system must be continuously monitored to ensure it is functioning as intended and that it can be revised or updated in response to changes in the operational environment.

- 😀 **Adaptability of Control Systems**: Internal controls should be flexible and adaptable to the evolving risks and changes within the organization to remain effective over time.

Q & A

What is the main focus of the lecture in this transcript?

-The main focus of the lecture is on the components of internal control systems, based on the framework for internal control and how these components operate and interact to ensure effective internal control.

Why is the identification of risks essential in the internal control process?

-Identifying risks is crucial because it helps in designing control activities that specifically address the identified risks, ensuring that the internal control system is targeted and effective in mitigating potential issues.

What role does the information and communication system play in internal control?

-The information and communication system is vital because it ensures the efficient dissemination of information, facilitating both the execution of transactions and the monitoring of internal control activities.

What are some of the key elements of an effective control environment?

-Key elements of an effective control environment include integrity, ethical values, commitment to competence, participation from the board of commissioners and audit committees, as well as the management's philosophy and operational style.

How does the risk assessment process begin in internal control systems?

-The risk assessment process begins by identifying factors that may cause risks, estimating the potential impact of those risks, determining the likelihood of their occurrence, and then establishing the necessary actions to mitigate or address the risks.

What are some examples of tasks that should be separated in the internal control process?

-Examples include separating the duties of those who manage assets (e.g., warehouse staff) from those who record transactions (e.g., accounting), separating transaction authorization from asset management (e.g., approving cash expenditures vs. cashier duties), and separating operational responsibilities from accounting tasks.

What is the difference between general authorization and specific authorization in internal control?

-General authorization refers to the overall approval for types of activities (e.g., budget spending), while specific authorization is needed for individual transactions, ensuring that each transaction is properly authorized before being executed.

Why are physical safeguards for assets and records important?

-Physical safeguards are important to prevent asset loss, damage, or theft. Assets and records should be stored securely, often in locked rooms or warehouses, to maintain their integrity and prevent unauthorized access.

What is the significance of independent checks in internal control?

-Independent checks are essential to ensure compliance with internal control procedures and to identify any deviations or weaknesses. They help verify that controls are being followed correctly and can highlight areas that need adjustment.

How should internal control systems be monitored over time?

-Internal control systems should be continuously monitored to ensure they are functioning as intended. If any component no longer aligns with operational requirements or if there are changes in the environment, the system should be reviewed and updated accordingly.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraVer Más Videos Relacionados

Pengendalian Intern

Auditing: Internal Controls and Risk Assessment

Model Blok Diagram Sistem Informasi Manajemen | Anshar Akil

Sistem Informasi Akuntansi #8 Sistem pengendalian internal & Sistem Informasi Akuntansi-Eko Triyanto

Principles of Internal Control Components

Sovereignty || Meaning, Definitions and Characteristics of Sovereignty || Deepika

5.0 / 5 (0 votes)