Principles of Internal Control Components

Summary

TLDRThis presentation delves into the principles of internal control, outlining five key components: control environment, risk assessment, control activities, information and communication, and monitoring activities. It emphasizes the importance of integrity, ethical values, board oversight, and management's role in setting structures and responsibilities. The script also addresses the significance of risk assessment, control activities, and effective communication within an organization. It concludes with a focus on monitoring and timely communication of internal control issues, tying everything back to the audit risk model.

Takeaways

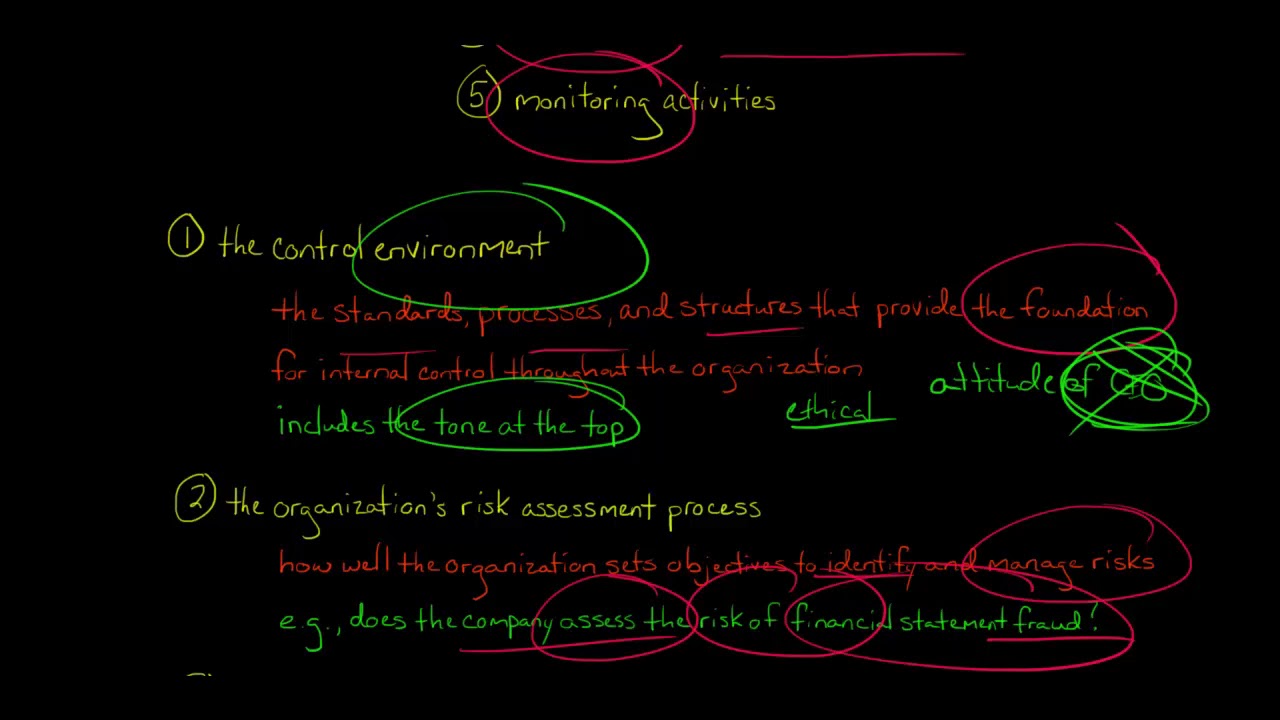

- 🏢 The control environment is foundational for internal control, emphasizing the organization's commitment to integrity and ethical values.

- 👥 Independence of the board of directors from management is crucial for effective oversight of internal control development and performance.

- 📊 Management's role in establishing structures, reporting lines, and defining authorities and responsibilities is key to pursuing organizational objectives.

- 👩💼 Attracting, developing, and retaining competent employees aligns with the organization's objectives and affects the internal control environment.

- 🔗 Holding individuals accountable for their internal control responsibilities ensures the pursuit of objectives and identifies those who fail to meet expectations.

- 🎯 Clear specification of objectives is essential for identifying and assessing related risks, which is a fundamental part of risk assessment.

- 🔍 Identifying and analyzing risks across the entity helps in planning how to manage and mitigate those risks effectively.

- 🚫 Considering the potential for fraud when assessing risks is important to establish an environment that reduces the likelihood of fraudulent activities.

- 🔄 Entities must assess and adapt to changes that could significantly impact the system of internal controls to maintain their effectiveness.

- 🛠️ Control activities are selected and developed to mitigate risks to an acceptable level, including performance reviews, physical controls, and segregation of duties.

- 💻 General control activities over technology are essential to support the achievement of objectives and often involve IT professionals for implementation.

- 📜 Establishing control activities through policies and procedures ensures that what is expected is put into practice within the organization.

- 📢 Quality information is crucial for the functioning of internal controls, including the accurate identification, classification, measurement, recording, and presentation of transactions.

- 🗣️ Effective internal communication regarding objectives and responsibilities for internal controls is necessary for their proper functioning.

- 🌐 External communication about issues affecting internal controls is important for transparency and addressing concerns with external parties.

- 🔍 Ongoing and separate evaluations are conducted to determine if internal control components are installed and functioning as intended.

- ⏰ Timely evaluation and communication of internal control problems to responsible parties are essential for corrective actions and improvements.

Q & A

What are the five components of internal control?

-The five components of internal control are the control environment, risk assessment, control activities, information and communication, and monitoring activities.

What is the first principle related to the control environment?

-The first principle related to the control environment is that the business shows a commitment to integrity and ethical values.

How does the board of directors demonstrate independence from management?

-The board of directors demonstrates independence from management by providing oversight over the development and performance of internal control.

What is the significance of management setting up structures, reporting lines, and authorities and responsibilities?

-Management setting up structures, reporting lines, and authorities and responsibilities is significant because it ensures that roles and responsibilities are well-defined, which is crucial for accountability and the smooth functioning of the organization.

Why is it important for a business to attract, develop, and retain competent employees?

-It is important for a business to attract, develop, and retain competent employees because it aligns with the organization's objectives and contributes to the overall performance and success of the business.

How does a business hold individuals accountable for their internal control responsibilities?

-A business holds individuals accountable by first determining the responsibilities for different individuals and then assessing whether they have followed through with their responsibilities. Those who do not meet expectations are held accountable.

What is the purpose of risk assessment in internal control?

-The purpose of risk assessment in internal control is to identify and assess risks related to objectives, which helps the business to manage those risks effectively.

Why is it necessary to consider the potential for fraud when assessing risks?

-Considering the potential for fraud when assessing risks is necessary to set up an environment within the organization that lessens the likelihood of fraud, which is part of the internal control components.

What is the role of control activities in mitigating risks to the achievement of objectives?

-Control activities play a role in mitigating risks by selecting and developing activities that contribute to reducing those risks to acceptable levels, ensuring the achievement of objectives.

How does a business ensure the quality of information used in internal controls?

-A business ensures the quality of information used in internal controls by obtaining, making, and using relevant and accurate information that supports the functioning of internal controls.

What is the significance of monitoring activities in internal control?

-Monitoring activities are significant in internal control because they involve ongoing evaluations to determine if the components of internal control are installed and functioning properly.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade Now

5.0 / 5 (0 votes)