Akuntansi Pertanggungjawaban

Summary

TLDRThis e-learning session focuses on responsibility accounting, a system used to track and report costs in organizations. The content explains key concepts such as defining responsibility accounting, the role of organizational structure, budgeting, cost categorization (controllable vs. uncontrollable costs), and the importance of regular cost reporting. With examples from a woodworking business, the script demonstrates how different levels of management are responsible for preparing and managing budgets, tracking actual costs, and analyzing variances. The session emphasizes the importance of clear accountability to optimize cost control and management performance.

Takeaways

- 😀 Responsibility accounting is a system designed to collect and report costs, ensuring accountability for cost deviations within an organization.

- 😀 Clear organizational structures are essential for responsibility accounting, with each management level having defined responsibilities for cost control.

- 😀 Costs are categorized into controllable and uncontrollable costs, allowing for more precise management and reporting.

- 😀 Budgeting is a key component of responsibility accounting, with each level of management required to prepare and manage its own budget.

- 😀 Cost control is not limited to production costs but extends to all costs within the company, including non-production expenses.

- 😀 Monthly cost variance reports are prepared to compare actual performance against budgeted costs, highlighting discrepancies and required actions.

- 😀 Responsibility accounting holds managers accountable for the costs in their areas of responsibility, ensuring better financial performance management.

- 😀 Variances in cost reports (both favorable and unfavorable) must be explained by the responsible managers to ensure transparency and proper management.

- 😀 A well-designed responsibility accounting system helps companies measure performance, optimize cost control, and enhance operational efficiency.

- 😀 The system also requires that managers understand both the planned and actual costs, enabling them to make data-driven decisions to improve organizational performance.

- 😀 Examples of cost categories within the company include material costs, labor costs, and overheads, which are reported and tracked at each management level for accountability.

Q & A

What is the primary purpose of responsibility accounting?

-The primary purpose of responsibility accounting is to track and report costs based on the responsibility of individual managers or departments within an organization. It helps assign accountability for cost variances and improves cost control and decision-making.

How does organizational structure play a role in responsibility accounting?

-An organizational structure establishes clear lines of authority and responsibility. Each level of management is assigned specific cost-related responsibilities, ensuring accountability for managing and reporting costs within their areas.

What are controllable and uncontrollable costs in responsibility accounting?

-Controllable costs are those that can be influenced by the manager responsible for a department or unit, such as materials and labor costs. Uncontrollable costs, on the other hand, cannot be directly influenced by the manager, such as overhead or corporate-level expenses.

Why is budgeting important in responsibility accounting?

-Budgeting is essential in responsibility accounting because it sets financial targets for each department or unit. It serves as a benchmark against which actual costs are measured, helping to identify variances and evaluate the performance of managers in controlling costs.

What are the key steps involved in applying responsibility accounting?

-The key steps include establishing an organizational structure with clear responsibilities, preparing budgets for each department, classifying costs into controllable and uncontrollable categories, collecting actual cost data, and comparing these to budgeted costs to assess performance.

How is cost information categorized and reported in responsibility accounting?

-Cost information is categorized based on whether it is controllable or uncontrollable by the responsible manager. Reports are generated periodically to compare actual costs with budgeted costs, and any variances are explained by the responsible managers.

What role do managers play in responsibility accounting reports?

-Managers are responsible for explaining any cost variances in responsibility accounting reports. They must take corrective actions if the actual costs exceed the budgeted costs, especially for controllable costs, and ensure that the department's financial performance aligns with organizational goals.

Can you give an example of how cost reporting works in a specific unit?

-For example, in a wood processing unit (Unit Pengolahan Kayu), the budget might set an expected cost for raw materials at Rp2,000,000, but the actual cost might be Rp2,100,000, resulting in a variance of Rp100,000. The manager must explain this variance and make adjustments as necessary.

What is the significance of a cost code system in responsibility accounting?

-A cost code system organizes costs by categorizing them into specific codes. This system helps ensure that costs are tracked efficiently and effectively, making it easier to assign responsibility for each cost item to the appropriate manager.

How does responsibility accounting contribute to performance evaluation?

-Responsibility accounting contributes to performance evaluation by providing clear data on how well each manager controls costs within their area. Managers are evaluated based on their ability to meet budgeted targets and manage variances, helping identify areas for improvement or corrective actions.

Outlines

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنMindmap

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنKeywords

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنHighlights

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنTranscripts

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنتصفح المزيد من مقاطع الفيديو ذات الصلة

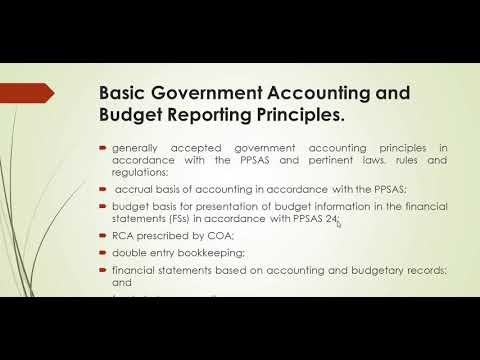

Introduction to Government Accounting

Activity Based Management 1

What Is SOCIAL ACCOUNTING? SOCIAL ACCOUNTING Definition & Meaning

SAP FICO Full Tutorial in Hindi | SAP FICO for Beginners | SAP INTRODUCTION

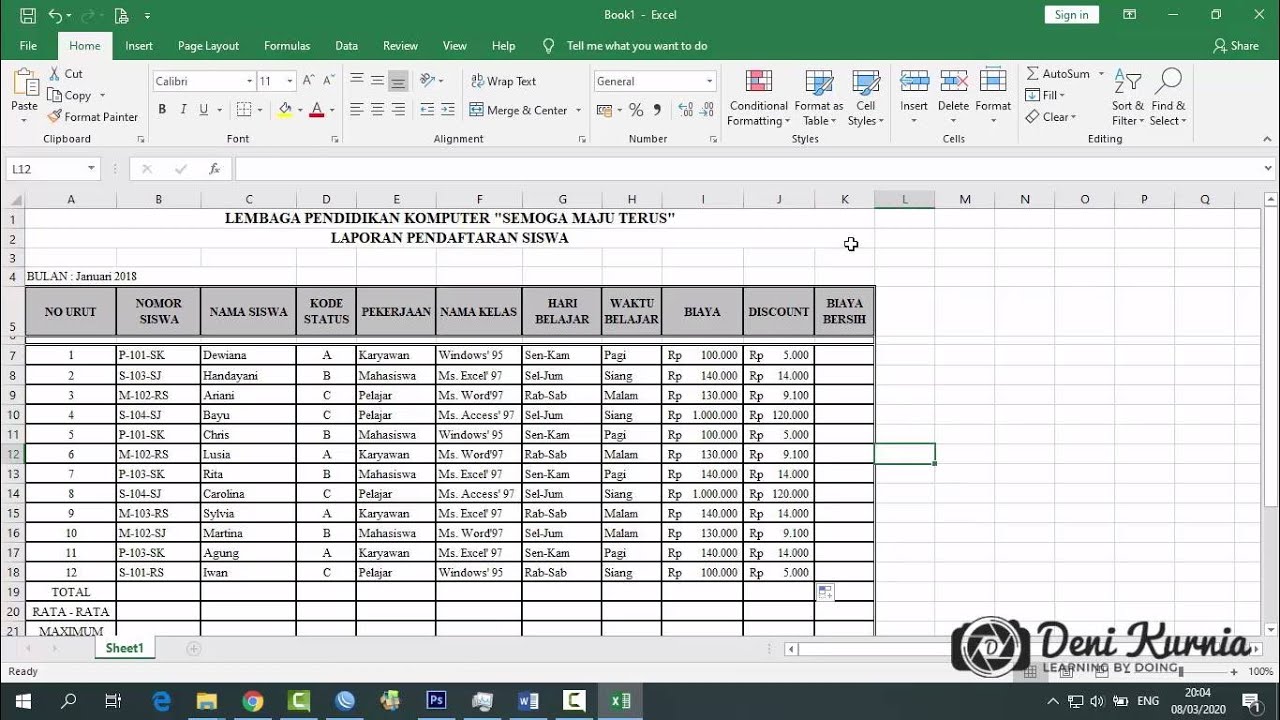

Pembahasan Soal UKK Akuntansi 2019/2020 - Soal 2 Spreadsheet

Emphasis of matter or Other Matter paragraph Audit Report

5.0 / 5 (0 votes)