Balance Sheet

Summary

TLDRThis script offers an insightful overview of a company's balance sheet, distinguishing between assets—both tangible and intangible—and liabilities. It delves into the concepts of liquidity, equity, and the operating cycle, illustrating how these components interplay to reflect a company's financial health. The script uses real-world examples to clarify complex financial terms and emphasizes the importance of maintaining balance in a company's financial structure.

Takeaways

- 🏢 Assets are economic resources a company owns, including both tangible (e.g., buildings, machinery) and intangible (e.g., patents, trademarks) assets.

- 💧 Liquidity refers to how easily an asset can be converted to cash without affecting its price, with cash being the most liquid and real estate being less so.

- 📊 Liabilities are the debts or obligations a company owes to external parties, such as bank loans or advance payments from customers.

- 📈 Equity represents the residual interest in a company's assets after liabilities are deducted, showing the owner's claim on the company's assets.

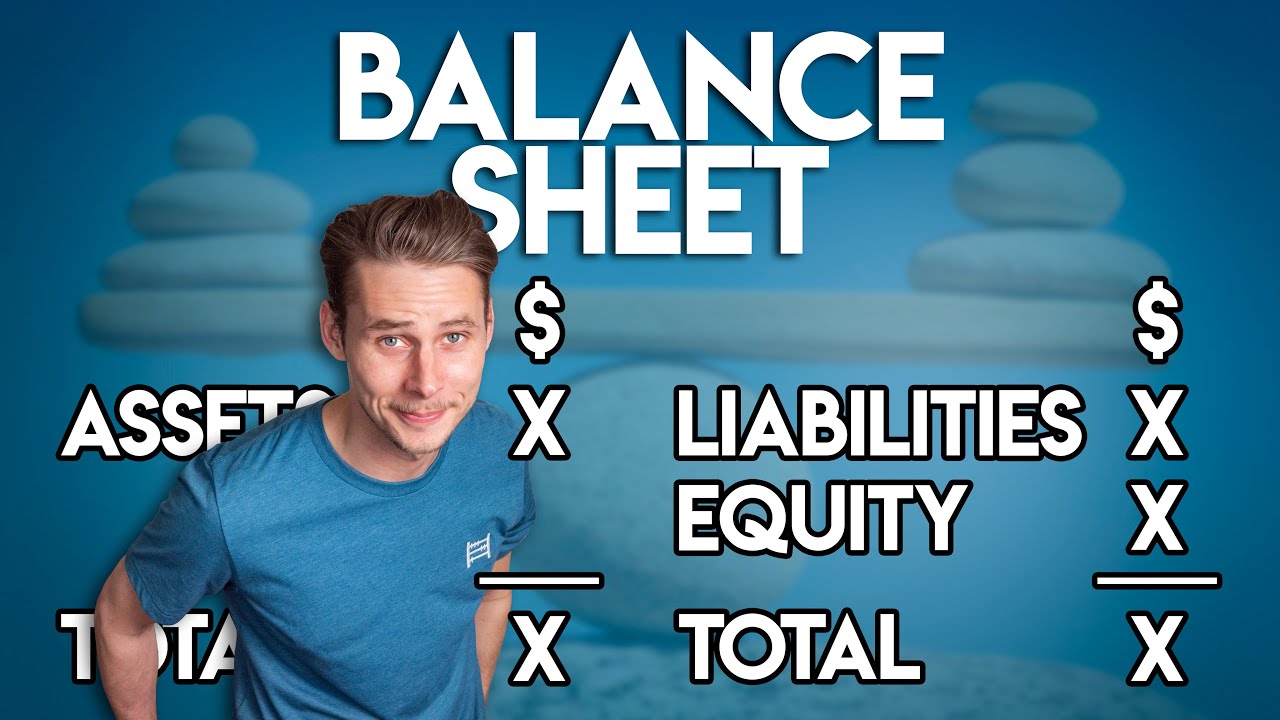

- 📋 The balance sheet lists assets on the left, liabilities and equity on the right, reflecting the uses of capital and the sources of capital.

- 🔄 The operating cycle describes the journey of money in a business, from spending on products to sales and receiving payments.

- 📈 Non-current assets are long-term assets expected to provide benefits beyond one year, such as property, plant, and equipment (PPE).

- 📦 Current assets are expected to be converted into cash or used up within one year or the operating cycle, including inventory and financial assets.

- 💼 Goodwill represents the premium paid over the fair value of an asset, while intangible assets include intellectual property, patents, and licenses.

- 💡 Non-current tax assets can result from overpayments or advance payments of taxes, potentially offsetting future tax liabilities.

- 💸 Current liabilities include short-term obligations due within a year, such as lease payments, trade payables, and other financial liabilities.

- 📉 Insolvency means lacking the financial resources to meet debt obligations, which can occur even if a company is liquid but has an unstable financial position.

Q & A

What are the two main types of assets mentioned in the script?

-The two main types of assets mentioned are tangible assets, such as buildings, machinery, and furniture, and intangible assets, which include patents, trademarks, copyrights, software licenses, prepaid leases, and franchise contracts.

What does liquidity mean in the context of assets?

-Liquidity refers to the ease with which an asset can be converted into cash without significantly affecting its price. High liquidity means an asset can be quickly sold at a stable price, while low liquidity implies it may take longer to sell, potentially requiring a discount in the price.

Why are cash and stocks of large companies considered liquid assets?

-Cash and stocks of large companies are considered liquid assets because they can be quickly sold at a stable price due to their high trading frequency and volume in the market.

What is the difference between assets and liabilities on a balance sheet?

-Assets are the economic resources owned by a company, listed on the left side of the balance sheet, while liabilities are the obligations or debts that a company owes to external parties, listed on the right side.

What is the definition of equity on a balance sheet?

-Equity represents the residual interest in the assets of a company after deducting liabilities. It shows the owner's claim on the company's assets after the lenders have been paid off.

What are the typical components of equity mentioned in the script?

-The typical components of equity include share capital, which is the amount originally contributed by shareholders, and retained earnings, which are the cumulative amount of net income retained in the company after dividends have been paid out.

What is the operating cycle in a business?

-The operating cycle is the full journey of money in a business, starting from spending money to buy or produce products, making sales, and finally receiving payments from customers.

What are current assets and why are they important?

-Current assets are assets expected to be converted into cash or used up within one year or the operating cycle, whichever is longer. They are important because they represent the short-term liquidity and financial health of a company.

What does the term 'non-current assets' refer to?

-Non-current assets, also known as long-term assets, are assets expected to provide economic benefits beyond one year.

What is the difference between trade receivables and notes receivables?

-Trade receivables are amounts owed by customers for sales made on credit, while notes receivables refer to amounts owed by a client who needs more time to pay for a sale, usually involving a signed legal document and the charging of interest.

What is the significance of the balance sheet balancing?

-The balance sheet must balance to reflect the fundamental accounting equation that assets equal liabilities plus equity. If it doesn't balance, it indicates an error in accounting or data entry.

Outlines

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنMindmap

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنKeywords

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنHighlights

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنTranscripts

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنتصفح المزيد من مقاطع الفيديو ذات الصلة

5.0 / 5 (0 votes)