Internal Controls Framework

Summary

TLDRThis video introduces the Integrated Framework for Internal Controls, developed by the Committee of Sponsoring Organizations (COSO). It highlights five key components essential for building strong internal controls: control environment, risk assessment, control activities, information and communication, and monitoring activities. The framework, which is widely used across organizations, helps achieve objectives in operations, reporting, and compliance. It emphasizes the importance of leadership, ethical values, and collaboration at all levels. The video also encourages organizations to utilize COSO’s principles for effective internal control, ensuring a culture of accountability and integrity.

Takeaways

- 😀 The Integrated Framework for Internal Controls was developed by the Committee of Sponsoring Organizations (COSO) in 1992 and updated in 2013.

- 😀 The framework is widely used across organizations and businesses to establish effective financial management practices.

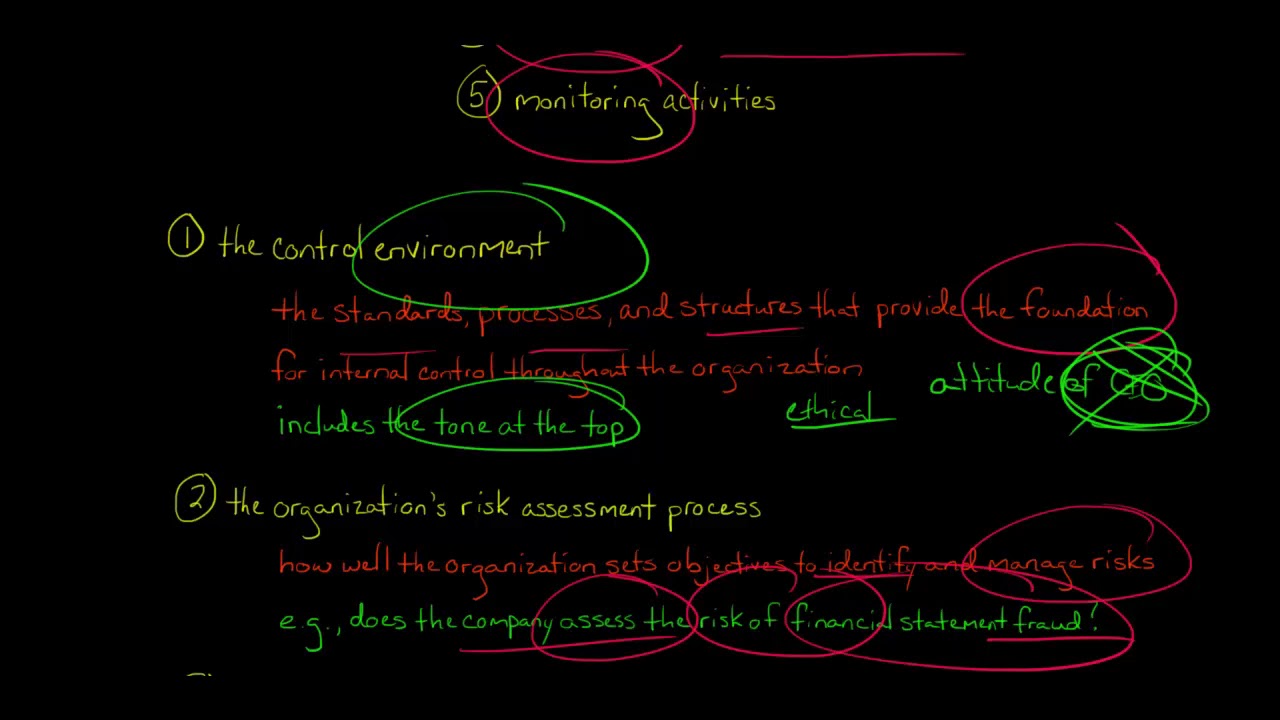

- 😀 The five key components of strong internal controls are: control environment, risk assessment, control activities, information and communication, and monitoring activities.

- 😀 The order of these components is important, and they must be implemented in a sequence, just like the foundation of a building.

- 😀 The components should not be viewed as separate; they work together as an integrated system with interdependent relationships.

- 😀 Control environment is the foundation of internal controls and is driven by ethical values, standards, and leadership at the top of the organization.

- 😀 Risk assessment involves identifying threats to the achievement of an organization’s objectives and accounting for changes in the internal and external environment.

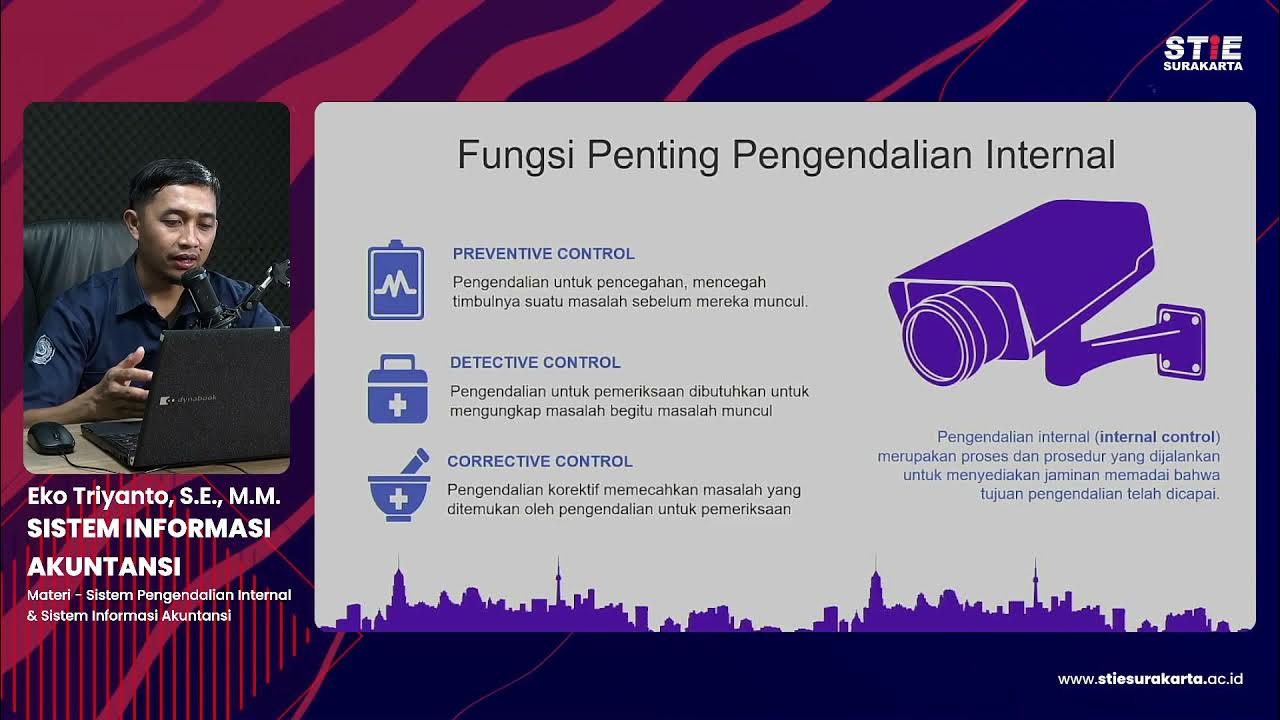

- 😀 Control activities include actions taken by management to mitigate risks and are carried out at all organizational levels.

- 😀 Information and communication ensure that necessary information flows throughout the organization and that employees understand their internal control responsibilities.

- 😀 Monitoring activities help identify ineffective policies and procedures and ensure that corrective actions are taken to address deficiencies.

- 😀 COSO’s integrated framework uses a three-dimensional cube to represent the five components, the objectives (operations, reporting, compliance), and the organizational structure.

- 😀 Strong internal controls require the involvement of all levels of the organization, and the 17 integrated framework principles guide effective implementation of the five components.

- 😀 For a deeper understanding of the 17 principles, refer to the handout available on the COSO website, linked in the video description.

Q & A

What is the Integrated Framework for Internal Controls?

-The Integrated Framework for Internal Controls is a structured approach developed by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) to help organizations design, implement, and maintain effective internal control systems.

When was the Internal Control Integrated Framework originally developed and updated?

-The framework was originally developed in 1992 by COSO and later updated in 2013 to reflect modern business practices and improve its relevance across different organizations.

What are the five key components of strong internal controls?

-The five key components are Control Environment, Risk Assessment, Control Activities, Information and Communication, and Monitoring Activities.

Why is the order of the internal control components important?

-The order matters because the components build upon one another. Just like constructing a building requires a foundation first, organizations must establish the control environment before effectively implementing the other components.

What is meant by the 'control environment' in an organization?

-The control environment refers to the ethical values, standards, organizational structures, and processes that shape how internal controls operate. It is often described as the 'tone at the top' set by leadership.

What is the purpose of risk assessment in internal controls?

-Risk assessment helps organizations identify and evaluate potential threats that could prevent them from achieving their objectives, including risks arising from internal and external changes.

What are control activities and why are they important?

-Control activities are the actions and procedures implemented by management to reduce risks and ensure organizational objectives are achieved. They occur at all levels of the organization and throughout business processes.

What is an example of a key control activity mentioned in the script?

-A key example is the separation of duties, which ensures that no single person is responsible for multiple roles in an accounting process, reducing the risk of errors or fraud.

How do information and communication support internal controls?

-Information and communication ensure that necessary data and responsibilities related to internal controls are clearly conveyed throughout the organization, helping personnel understand and fulfill their roles.

What role do monitoring activities play in the internal control framework?

-Monitoring activities involve regularly evaluating internal control processes to identify deficiencies and ensure policies, procedures, and practices are functioning effectively.

What are the three main objectives represented in the COSO internal control cube?

-The three objectives are Operations (efficiency and effectiveness of activities), Reporting (reliability and transparency of financial and non-financial reports), and Compliance (adherence to laws and regulations).

What does the third dimension of the COSO cube represent?

-The third dimension represents different levels of an organization’s structure, such as individual units, divisions, operational units, or functional areas, emphasizing that internal controls apply across all organizational levels.

What are the 17 principles within the Integrated Framework?

-The 17 principles represent fundamental concepts tied to the five internal control components and provide guidance for organizations to effectively design and implement a complete internal control system.

Why is internal control considered a shared responsibility?

-Internal control requires participation from all levels of the organization, including leadership, management, and employees, because each individual plays a role in maintaining effective controls and supporting organizational objectives.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级浏览更多相关视频

The 5 Components of Internal Control

Internal Control Basics | Principles of Accounting

All about the COSO framework

Auditing: Internal Controls and Risk Assessment

Sistem Informasi Akuntansi #8 Sistem pengendalian internal & Sistem Informasi Akuntansi-Eko Triyanto

Control Frameworks: COSO & COBIT | Fundamentals of Internal Auditing | Part 5 of 44

5.0 / 5 (0 votes)