PPh Orang Pribadi (Update 2023) - 8. PPh UMKM (PP 23) untuk WPOP

Summary

TLDRIn this video, the speaker explains the key aspects of PP 23 of 2018, which focuses on final income tax (PPH final) for UMKM. The tax benefits under this regulation apply specifically to businesses, not freelance professions. The speaker outlines various professions excluded from these benefits, such as lawyers, doctors, artists, and others. The tax rate is set at 0.5% of gross turnover, with a threshold of 500 million IDR in annual revenue. The video also highlights how the tax is applied to incremental income once the threshold is exceeded. Finally, the speaker encourages viewers to like, subscribe, and support an upcoming practical tax training.

Takeaways

- 😀 PP 23 of 2018 provides a final income tax (PPH Final) scheme for Micro, Small, and Medium Enterprises (UMKM) in Indonesia.

- 😀 Only businesses (usaha) are eligible for the PP 23 tax benefits, while personal services (pekerjaan bebas) are excluded from this facility.

- 😀 Personal service professions like lawyers, accountants, doctors, and entertainers are specifically excluded from the PP 23 tax benefits.

- 😀 The tax rate under PP 23 is 0.5% of gross revenue (omzet), and it applies to businesses once their turnover exceeds IDR 500 million annually.

- 😀 The PP 23 scheme is available for up to **7 years** for qualifying businesses, after which normal tax calculation methods apply.

- 😀 Revenue below IDR 500 million annually is exempt from PP 23 tax, and businesses will only be taxed when their turnover exceeds this threshold.

- 😀 When a business's revenue exceeds IDR 500 million, only the portion of the revenue above this limit is subject to the 0.5% tax rate.

- 😀 For example, if a business earns IDR 200 million in January, it is not taxed, but in March, when turnover exceeds the IDR 500 million threshold, the excess amount is taxed at 0.5%.

- 😀 If a business’s turnover reaches IDR 500 million, the tax will be calculated on the portion above this limit, e.g., IDR 100 million above the threshold would be taxed at 0.5%.

- 😀 The PP 23 tax scheme helps simplify tax obligations for small businesses by applying a flat 0.5% rate on gross revenue once the revenue threshold is crossed.

- 😀 The recent change under the HPP Law ensures that businesses with turnover under IDR 500 million do not need to pay tax under PP 23, making it more accessible for small businesses to comply.

Q & A

What is PP 23 of 2018 about?

-PP 23 of 2018 refers to a regulation about the final income tax (PPH) for Small and Medium Enterprises (UMKM) in Indonesia. It outlines the tax provisions for individuals engaged in business activities.

Who is eligible for the PP 23 tax facilities?

-Only individuals engaged in business activities are eligible for the PP 23 tax facilities. Freelancers or professionals providing services like lawyers, consultants, and doctors are excluded from these facilities.

What is the main distinction between 'usaha' (business) and 'pekerjaan bebas' (freelance work) in the context of PP 23?

-'Usaha' refers to business activities, which are eligible for the PP 23 facilities, while 'pekerjaan bebas' refers to freelance work or independent services (e.g., lawyers, doctors, consultants), which are excluded from these tax facilities.

What are some examples of 'pekerjaan bebas' that are excluded from PP 23?

-Examples of 'pekerjaan bebas' include professions like lawyers, accountants, consultants, notaries, doctors, architects, artists, athletes, and teachers, among others.

What is the tax rate under PP 23?

-The tax rate under PP 23 is 0.5% of the gross income (omset) for eligible individuals engaged in business activities.

How long can an individual benefit from the PP 23 tax facility?

-An individual can benefit from the PP 23 tax facility for a maximum of 7 years. After this period, they must switch to regular tax calculations.

What is the threshold for PP 23 taxation, as stated in the recent tax law update?

-The threshold for PP 23 taxation starts from a gross income (omset) of 500 million IDR. Businesses with a gross income up to 500 million IDR are exempt from PP 23, but those exceeding this amount will be taxed at 0.5%.

How is the tax calculated for businesses with a gross income exceeding 500 million IDR?

-For businesses with a gross income exceeding 500 million IDR, the tax is calculated as 0.5% of the gross income above the 500 million IDR threshold. For example, if the business makes 200 million IDR after reaching 500 million, the tax will be 0.5% of that additional 200 million IDR.

What happens if a business's gross income does not reach 500 million IDR?

-If a business's gross income is below 500 million IDR, it is not subject to PP 23 taxation. The tax only applies once the business's income exceeds this threshold.

What is the significance of the 500 million IDR threshold in the PP 23 tax scheme?

-The 500 million IDR threshold represents the point at which a business becomes liable for PP 23 taxation. Businesses with incomes below this threshold are exempt, but those with incomes above it will face a 0.5% tax on their gross income.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级浏览更多相关视频

Belajar Pajak untuk UMKM (PPh Final/PP23 2018)

2 PPh Pasal 4 ayat 2 : Objek, Pelunasan, Pelaporan

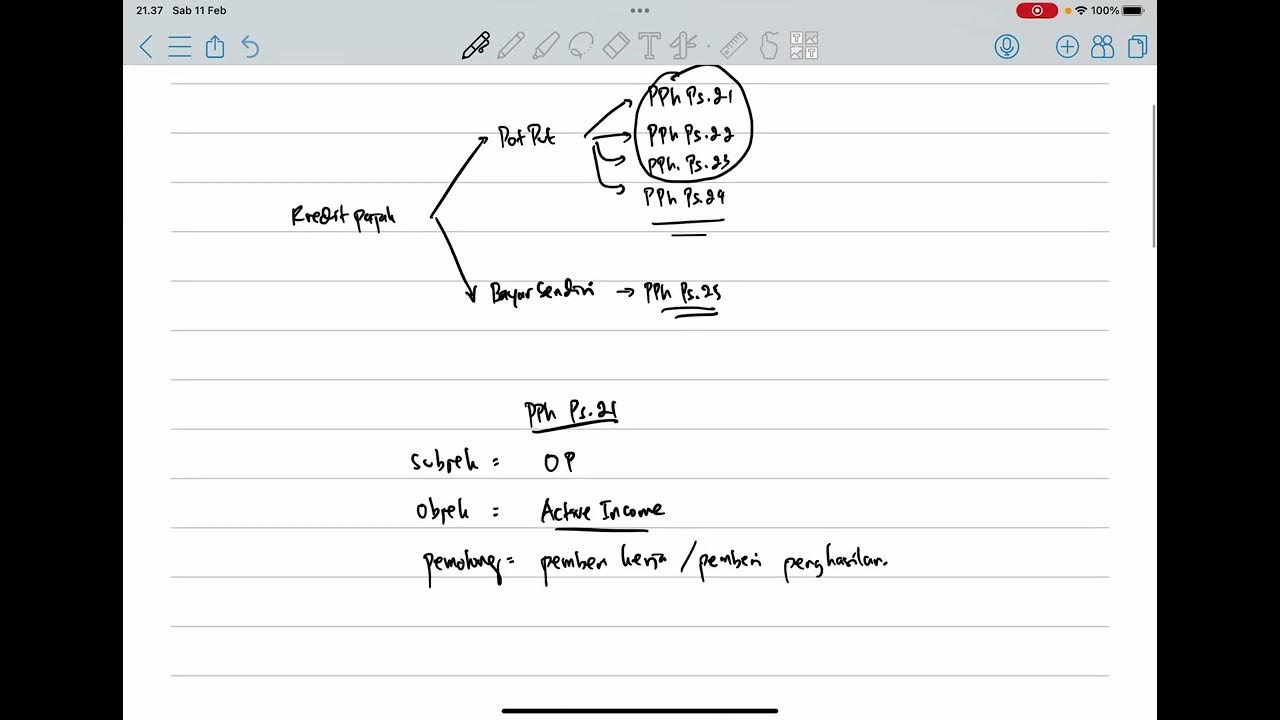

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

PPh Orang Pribadi (Update 2023) - 13. Panduan Pengisian SPT 1770 (Status KK)

Pertanyaan Saat Interview Staff Pajak #interview #tax #staff

Apa itu Pajak Final? Apa bedanya PPh Final dan PPh Non-Final? | #Paham Pajak

5.0 / 5 (0 votes)