#Part1 Ch 18 Revenue Recognition Akuntansi Keuangan Menengah II

Summary

TLDRThis educational video on Intermediate Financial Accounting focuses on the recognition and measurement of revenue, as detailed in Chapter 18 of the textbook. The video explores the five-step process for revenue recognition, emphasizing the importance of understanding contracts with customers and performance obligations. It introduces the latest accounting standards, such as PSAK 72 in Indonesia, and discusses the asset-liability approach to revenue recognition. The key steps include identifying the contract, determining performance obligations, and recognizing revenue when control is transferred to the customer, with practical examples such as the sale of aircraft.

Takeaways

- 😀 PSAK 72, which governs revenue recognition from contracts with customers in Indonesia, was adopted from IFRS and is applicable since January 1, 2020.

- 😀 The new revenue recognition standard aims to improve the quality of financial reporting and resolve issues in previous standards by eliminating contradictions and inefficiencies.

- 😀 PSAK 72 applies to all contracts with customers, except for those related to leases, insurance contracts, financial instruments, and non-monetary exchanges.

- 😀 The standard uses an 'asset-liability approach' to recognize revenue, focusing on the obligations and assets involved in a contract with a customer.

- 😀 Revenue recognition is based on five key steps: identifying the contract, identifying performance obligations, determining the transaction price, allocating the transaction price, and recognizing revenue.

- 😀 A contract is defined as an agreement between two or more parties that creates enforceable rights and obligations, which can be written or oral.

- 😀 Performance obligations are promises to transfer goods or services, and they can be distinct or combined, depending on the terms of the contract.

- 😀 The transaction price refers to the amount expected to be received from a contract, considering any variable elements such as discounts or incentives.

- 😀 If a contract includes multiple performance obligations, the transaction price must be allocated among them based on their relative standalone selling prices.

- 😀 Revenue is recognized when a performance obligation is satisfied, meaning control of the goods or services has transferred to the customer, signaling the completion of the obligation.

Q & A

What is the main focus of Chapter 18 in the book 'Kisuikan Marvel'?

-Chapter 18 primarily focuses on the recognition and measurement of revenue, including the fundamental concepts behind revenue recognition and the five-step process involved in recognizing revenue from contracts with customers.

What is the significance of the 5-step process in revenue recognition?

-The 5-step process is essential in recognizing revenue. It includes identifying the contract with the customer, determining performance obligations, setting the transaction price, allocating the transaction price, and recognizing revenue when performance obligations are satisfied.

What is the role of PSAK 72 in Indonesia regarding revenue recognition?

-PSAK 72 in Indonesia is the standard for recognizing revenue from contracts with customers. It was adopted from the IFRS standard, and it provides a comprehensive framework that replaces various previous standards, including PSAK 23 and PSAK 34.

What does the term 'Asset Liability Approach' refer to in PSAK 72?

-The Asset Liability Approach refers to recognizing revenue based on the analysis of assets and liabilities arising from contracts with customers. This approach considers the obligations that a company has toward the customer and the rewards it receives from the customer.

What are the exclusions from the scope of PSAK 72?

-PSAK 72 does not apply to certain types of contracts such as leases (PSAK 73), insurance contracts (PSAK 74), financial instruments (PSAK 71), and non-monetary exchanges.

What are the main objectives of PSAK 72 in terms of revenue recognition?

-PSAK 72's main objectives are to set principles for recognizing the nature, amount, timing, and uncertainty of revenue and cash flows from contracts with customers, ensuring revenue reflects the transfer of goods or services to customers.

How does the concept of 'Performance Obligation' relate to revenue recognition?

-A Performance Obligation refers to a promise made in a contract to transfer goods or services to a customer. It is essential in determining when revenue is recognized. If performance obligations are satisfied, the company recognizes the revenue.

What does 'Transaction Price' mean in the context of PSAK 72?

-Transaction Price refers to the amount of consideration expected to be received in exchange for transferring goods or services to the customer. It is determined after identifying the performance obligations.

Can you explain the fifth step in the revenue recognition process?

-The fifth step is the actual recognition of revenue when a company has fulfilled its performance obligations. This occurs when control of the goods or services is transferred to the customer, indicating the company’s obligation has been satisfied.

How does the example of Airbus selling a plane to Cathay Pacific Airlines illustrate the five-step process?

-In the Airbus example, the process starts with identifying the contract with the customer, followed by determining the performance obligation (delivery of the plane), setting the transaction price (100 million euros), allocating the transaction price if necessary, and finally recognizing revenue when the plane is delivered and control passes to the customer.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级浏览更多相关视频

Accounting Principles | Class 11 | Accountancy | Chapter 3 | Part 2

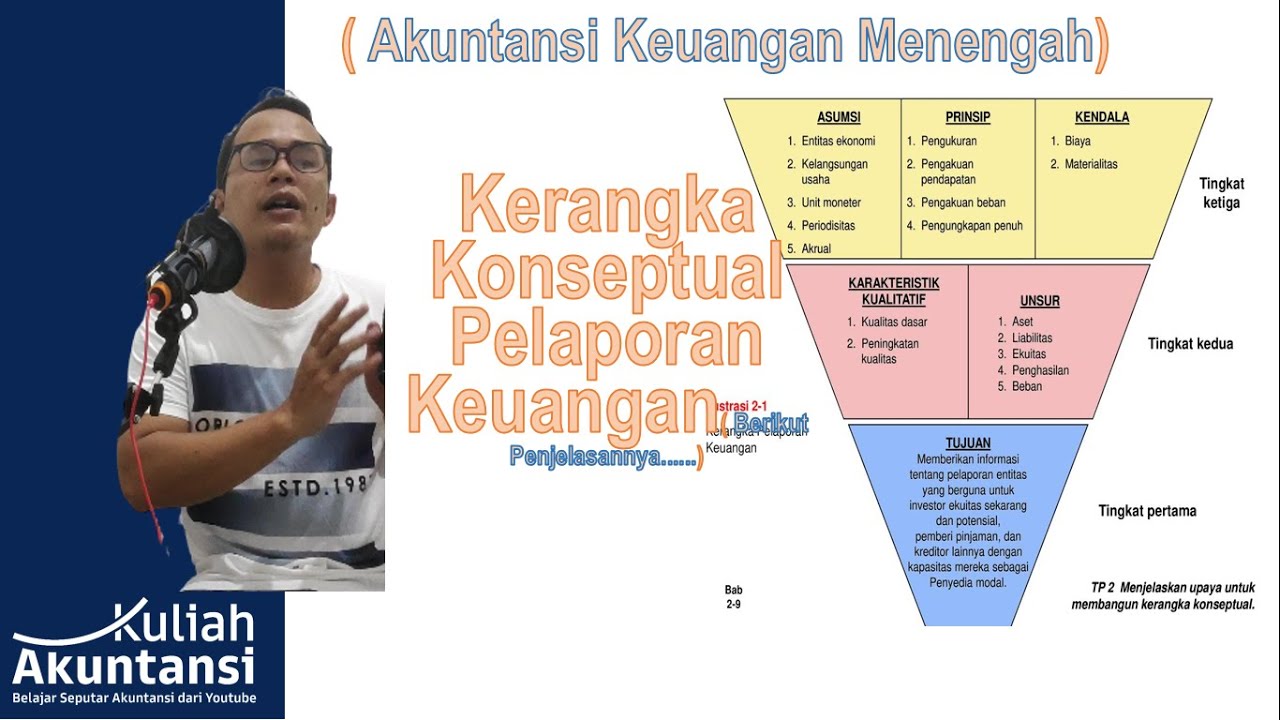

Akuntansi Keuangan Menengah : Kerangka Konseptual Pelaporan Keuangan

Chapter 5: Recognition and Derecognition

[Financial Accounting]: Chapter 3: The Adjusting Process

Pengakuan dan pengukuran piutang

#part1 Ch 17 Investment - Akuntansi Keuangan Menengah 2

5.0 / 5 (0 votes)