She Did, Too! $28,000+ In Credit Card Debt Pays Off Within 6 Months

Summary

TLDRIn this finance tutorial, Christy van from Fantastic Finances shares a strategy to quickly eliminate credit card debt. The case study involves an author with fluctuating income who consolidates her debt using a personal line of credit, reducing her monthly payments and focusing on paying off the principal. By strategically managing her cash flow and minimizing interest payments, she successfully clears nearly $330,000 in debt within six months, highlighting the power of financial planning and debt management.

Takeaways

- 😀 The video is about a financial advice channel by Christy van, focusing on managing and reducing credit card debt.

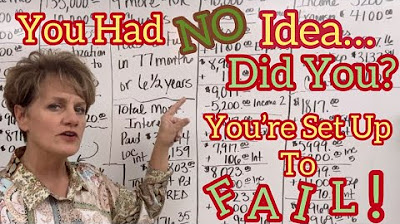

- 📚 The scenario involves an author with fluctuating income, averaging at $9,000 a month, and significant credit card debt.

- 💳 The author has four credit cards with various balances and monthly payments, totaling $1,900 in debt payments.

- 💼 The author's monthly expenses, including rent, are $2,772, leaving her with approximately $4,300 in cash flow.

- 🏦 Christy suggests using a personal line of credit to consolidate the credit card debt, which would free up cash flow and reduce interest payments.

- 🔢 The author is advised to start by consolidating two Capital One cards and part of the Chase card, totaling $9,677.

- 💰 By transferring income into the line of credit, the author satisfies the monthly payment, reducing the balance and freeing up cash flow.

- 📈 The strategy involves gradually paying down the Chase card and then focusing on the Discover card, reducing the overall debt balance each month.

- 🚀 The author is projected to eliminate almost $30,000 in debt within six months by strategically managing her finances and using a line of credit.

- 💡 The video emphasizes the importance of eliminating high-interest credit card payments and using cash flow to reduce debt more efficiently.

- 🌟 Christy encourages viewers to learn financial strategies to save on interest and invest in their future, rather than paying banks.

Q & A

What is the main topic of the video?

-The main topic of the video is about managing credit card debt and using a personal line of credit to consolidate and pay off debt more efficiently.

Who is the author of the video script?

-The author of the video script is Christy Van, who hosts the channel 'Fantastic Finances'.

What is the average monthly income of the author mentioned in the script?

-The author's average monthly income is stated to be $9,000, though it can vary between $7,000 and $177,000.

How many credit cards does the author mention in the script?

-The author mentions four credit cards in total: one Chase, one Discover, and two Capital One cards.

What is the strategy used in the script to manage the credit card debts?

-The strategy involves obtaining a personal line of credit, transferring the credit card balances to it, and then using the author's income to pay down the balance and reduce interest payments.

What is the total amount of credit card debt the author initially has?

-The total initial credit card debt is the sum of the Chase card at $14,437, Discover at $7,710, and two Capital One cards at $5,459 and $3,118, which amounts to approximately $30,724.

What is the approximate monthly cash flow the author has after expenses and debt payments?

-After expenses and debt payments, the author has approximately $4,300 in monthly cash flow.

How much interest would be charged monthly on the line of credit with an 11% interest rate, based on the highest balance?

-Based on the highest balance of $9,677, the interest charged would be approximately $89 per month, but this is an estimate as the actual interest would be calculated on the average daily balance.

What is the final balance on the Chase account after the author's strategy is implemented?

-After implementing the strategy, the final balance on the Chase account is reduced to zero.

How does the author suggest using the freed-up cash flow after eliminating the credit card debts?

-The author suggests using the freed-up cash flow to revolve expenses and save for future purchases or investments.

What is the author's advice for those struggling with credit card debt payments?

-The author advises to stop making high-interest credit card payments and instead use a personal line of credit to consolidate and reduce the debt more strategically.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Paying off $30k in debt made EASY with the right tools. Velocity Banking = Financial Peace

You’re Not Poor…You’re Getting ROBBED!

I Will Teach You To Be Rich by Ramit Sethi - How You Become Rich ► Animated Book Summary

How to Pay Off Your Maxed Out Credit Cards with ZERO Cashflow!!!| @JustJWoodfin

How to Pay Off A Credit Card with 0 Cash Flow!

How we got hooked on credit cards - Nidhi Upadhyaya

5.0 / 5 (0 votes)