Game Theory and Oligopoly: Crash Course Economics #26

Summary

TLDRThis Crash Course Economics episode delves into competition and game theory, explaining different market structures like perfect competition, monopoly, monopolistic competition, and oligopoly. It highlights how oligopolies, controlled by a few companies, engage in non-price competition and use game theory to make strategic decisions, illustrated with the 'prisoner's dilemma' and real-world examples like airline baggage fees. The video also discusses collusion, cartels, and the use of payoff matrices to predict outcomes in competitive scenarios.

Takeaways

- 🎓 Economics discusses competition and game theory, which are essential for understanding market structures and strategic decision-making.

- 🌟 There are four types of market structures: perfect competition, monopolies, monopolistic competition, and oligopolies, each with distinct characteristics.

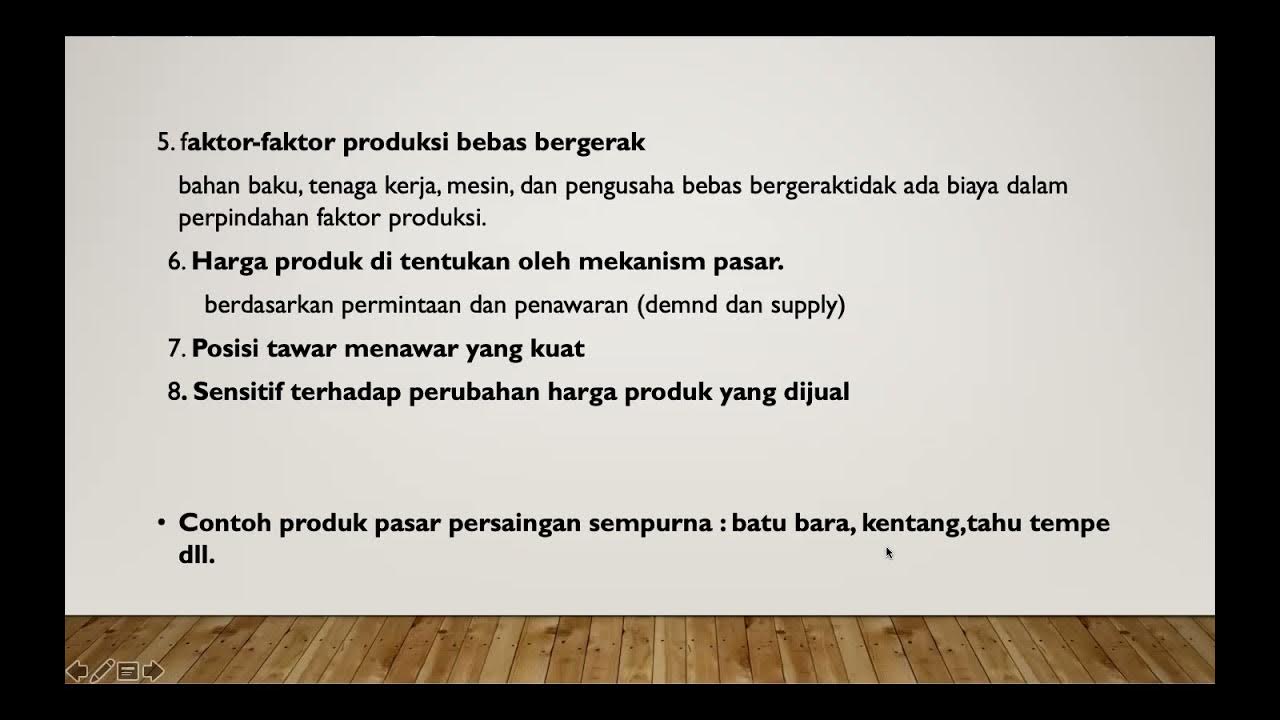

- 🍓 Perfect competition is characterized by many producers, identical products, and easy entry, such as in the agricultural market for strawberries.

- 🏭 A monopoly is a market dominated by a single company with high barriers to entry, giving it significant control over pricing.

- 🍔 Monopolistic competition involves many producers with similar but not identical products, like fast food chains, where companies can slightly vary their prices.

- 💻 Oligopolies are controlled by a few large companies with high barriers to entry, such as in the computer and mobile phone markets.

- 💰 Non-price competition is a strategy used in oligopolies where companies compete on factors like style, quality, location, or service rather than price.

- 📺 Advertising is a prominent form of non-price competition, where companies spend heavily to differentiate themselves and stand out in the market.

- 🤔 Game theory, including the 'prisoner's dilemma,' helps explain why companies make decisions based on the actions of their competitors and the potential outcomes.

- 💡 The concept of 'price leadership' in oligopolies can be a legal form of companies following each other's price changes, but it can be difficult to distinguish from illegal collusion.

- 📈 Payoff matrices in game theory illustrate the potential outcomes for companies based on their strategic decisions, highlighting the challenges of achieving optimal results.

- 🛒 Healthy competition, driven by game theory insights, can lead to innovation and better products for consumers, but it can also result in winners and losers in the market.

Q & A

What is the main topic discussed in this Crash Course Economics video?

-The main topic discussed in this video is competition and game theory, specifically focusing on different market structures and how companies in oligopolies use non-price competition and game theory to make strategic decisions.

What are the four types of market structures mentioned in the script?

-The four types of market structures mentioned are perfect competition, monopoly, monopolistic competition, and oligopoly.

Why do individual businesses in a perfectly competitive market have no control over prices?

-Individual businesses in a perfectly competitive market have no control over prices because there are many producers offering identical products, and new businesses can easily enter the market, which prevents any single producer from influencing the market price.

What is the difference between monopolistic competition and an oligopoly?

-Monopolistic competition is a market with many producers, relatively low barriers to entry, and products that are similar but not identical. An oligopoly, on the other hand, is a market controlled by a few large companies with high barriers to entry, and the products may be similar but are not identical.

How do companies in an oligopoly typically compete with each other without changing prices?

-Companies in an oligopoly typically compete through non-price competition, which includes focusing on style, quality, location, service, and advertising to distinguish their products from competitors.

What is the 'prisoner's dilemma' in game theory and what does it illustrate?

-The 'prisoner's dilemma' is a classic game theory scenario where two individuals, when unable to communicate, make decisions that may not result in the best collective outcome due to a lack of cooperation, even though it seems rational from an individual perspective.

Why do companies in an oligopoly often end up with similar prices for their products?

-Companies in an oligopoly often end up with similar prices because if one company lowers its price, others are likely to follow to remain competitive, resulting in a shared customer base and reduced profits. If they raise prices, they risk losing customers to competitors or attracting new entrants to the market.

What is the difference between collusion and price leadership in the context of oligopolies?

-Collusion refers to illegal agreements between companies to fix prices or other market conditions to their mutual benefit, often at the expense of consumers. Price leadership is when one company changes its prices and others follow suit without explicit collusion, which is technically legal but can be difficult to distinguish from collusion.

What is a payoff matrix in the context of game theory?

-A payoff matrix is a tool used in game theory to illustrate the possible outcomes and profits for each player in a strategic interaction, based on the different strategies they might choose.

Why is advertising so prevalent in industries with oligopolies?

-Advertising is prevalent in industries with oligopolies because companies need to differentiate themselves from competitors without changing prices. Advertising helps create brand awareness and loyalty, which can influence consumer choices and justify premium pricing.

What is the role of antitrust laws in preventing collusion and promoting competition?

-Antitrust laws are designed to prevent collusion and maintain fair competition by regulating anti-competitive practices such as price-fixing, market-sharing, and other forms of collusion that can harm consumers and stifle innovation.

How can game theory help companies make strategic decisions in oligopolistic markets?

-Game theory helps companies anticipate the actions of their competitors and make strategic decisions that maximize their profits. By understanding the potential outcomes and the best responses to different scenarios, companies can develop strategies that account for the interdependence of their market decisions.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

5.0 / 5 (0 votes)