MGT101_Topic005

Summary

TLDRThis video explains the five key elements of financial statements: assets, liabilities, owner equity, incomes, and expenses. The speaker highlights the importance of accurately classifying financial information, as mistakes in classification can lead to misleading financial analysis. Each element is defined, with assets being resources controlled by the entity, liabilities as present obligations, owner equity representing the owner’s stake, incomes as earnings, and expenses as costs incurred for benefits. Understanding these classifications is crucial for accurate financial reporting and avoiding errors that could impact the financial analysis.

Takeaways

- 😀 Financial information is classified into five main categories: assets, liabilities, owner equity, income, and expenses.

- 😀 Misclassifying financial information can lead to inaccurate financial statements and misleading financial analysis.

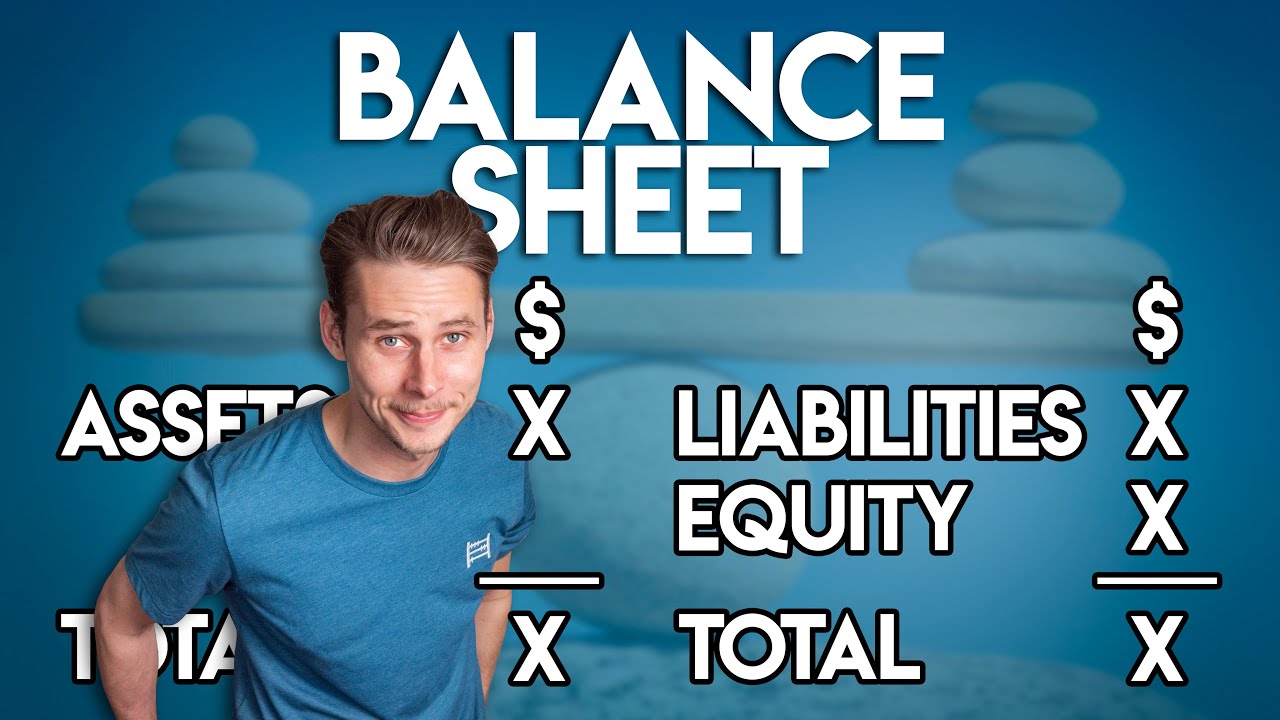

- 😀 Assets are resources under the control of the entity, not necessarily owned by it. A simple example is leased property, which is controlled by the entity but not owned.

- 😀 Assets are expected to generate future economic benefits, stemming from past events.

- 😀 Liabilities are the entity's present obligations that will likely require an outflow of resources in the future.

- 😀 Owner equity represents the financial stake of the entity's owners, including capital introduced and profits generated by the entity.

- 😀 Incomes refer to the earnings of the entity, while expenses represent the costs incurred in generating those earnings.

- 😀 The five main categories (assets, liabilities, owner equity, income, and expenses) also serve as the primary elements of financial statements.

- 😀 Each of the five main categories has subheads, which are the specific accounting heads under each classification.

- 😀 It is crucial to remember that liabilities refer to the obligations the entity must meet by the end of the reporting period.

- 😀 The classification of financial information into these categories ensures clarity and accuracy in financial reporting.

Q & A

What are the five main elements of financial statements?

-The five main elements of financial statements are Assets, Liabilities, Owner’s Equity, Incomes, and Expenses.

Why is it important to classify financial information correctly?

-Correct classification of financial information is crucial because mistakes in classification can lead to misleading financial statements and incorrect financial analysis, which could have destructive consequences.

What is the main distinction between assets and liabilities?

-Assets are resources controlled by the entity, expected to bring future economic benefits. Liabilities are the entity's current obligations, which will likely result in future outflows of resources.

Can an entity have assets without owning them? Provide an example.

-Yes, an entity can have assets without owning them. An example is leased property, which the entity controls but does not own.

How is owner's equity related to the capital introduced into the entity?

-Owner’s equity represents the owner’s stake in the entity, including both the capital the owner introduces into the business and the profits generated by the entity.

What is meant by the term 'economic benefits' in the context of assets and liabilities?

-Economic benefits refer to the potential inflows or outflows of resources that an entity expects to receive or give in the future, arising from past events or obligations.

What is the difference between incomes and expenses in financial statements?

-Incomes represent the earnings or revenues generated by the entity, while expenses are the costs incurred by the entity to generate those earnings.

What does the term 'future inflows of economic benefits' refer to in relation to assets?

-The term refers to the expected benefits, such as cash flows or other forms of economic value, that the entity will receive in the future from the use of its assets.

What are accounting heads and how do they relate to the five main heads of accounts?

-Accounting heads are subcategories under the five main heads of accounts (assets, liabilities, owner’s equity, incomes, and expenses). These subcategories help provide more detailed classification and organization of financial information.

What is the significance of 'present obligations' in liabilities?

-Present obligations refer to the entity’s responsibility to settle liabilities by transferring resources at the end of the reporting period, meaning the obligation exists at that moment and must be fulfilled in the future.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

5.0 / 5 (0 votes)