proses pencatatan dan pengakuan pembiayaan, investasi dan kewajiban di PPKD

Summary

TLDRThis video script explains the process of recording and recognizing financing, investments, and liabilities in government accounting. It covers various accounting practices such as financing receipts, investment entries, and liability recognition. Topics include the management of long-term investments, such as equity participation, and how they are documented in financial and budget journals. The script also discusses the distinction between short-term and long-term investments, the methods for reporting them, and the management of public finances to ensure transparency and accountability in accordance with regulations.

Takeaways

- 😀 Accounting for financing involves recording the receipt and expenditure of funds in government accounting journals.

- 😀 Financing receipts include the use of surplus budget calculations, loan receipts, bond sales, and loan repayments.

- 😀 Financing expenditures cover principal loan repayments, government capital contributions, and loan disbursements.

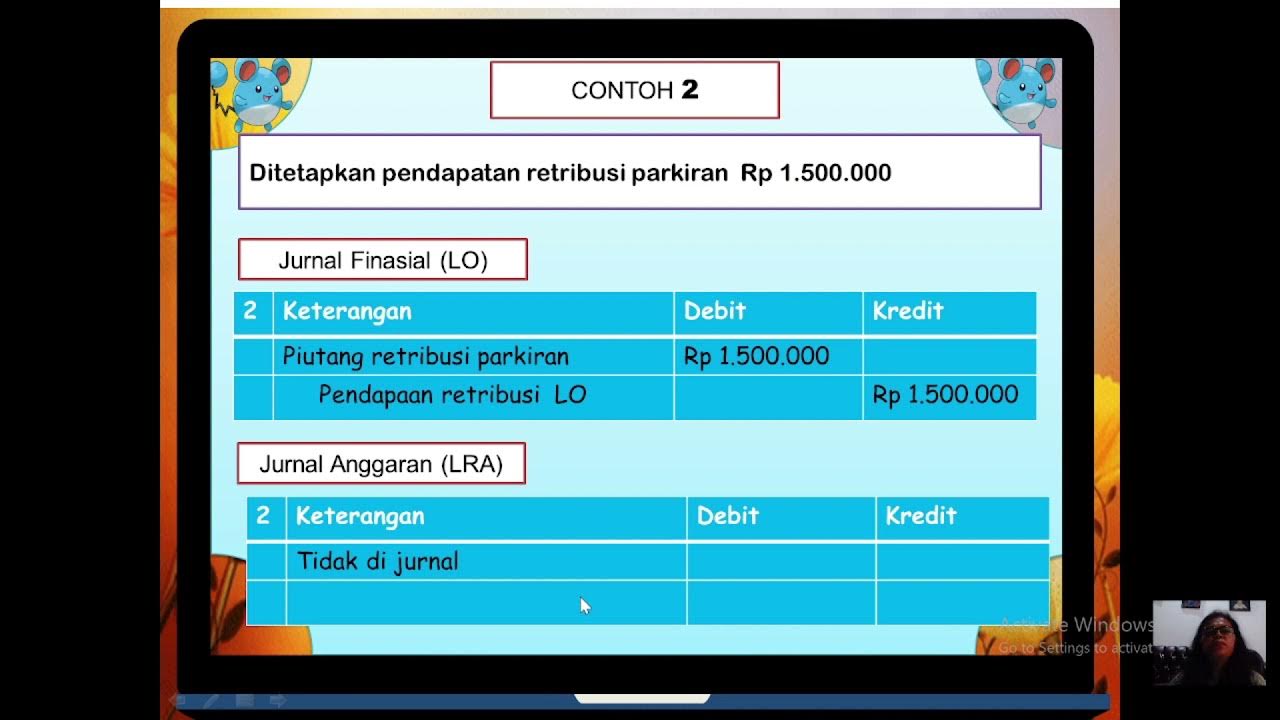

- 😀 Investment financing expenditure is recorded in long-term investment accounts in the financial journal, using debit entries for long-term investments and credit entries for cash.

- 😀 A government’s loan receipt is recorded as debt, and the financial journal reflects the cash receipt in the local government's account with corresponding debt recognition.

- 😀 Investment recognition includes recording short-term and long-term investments, with short-term investments reflected in short-term investment accounts and long-term investments in long-term investment accounts.

- 😀 Government investment income, including dividends and proceeds from investment management, is recorded as income or receivables in the financial journal.

- 😀 The release of government investments is recorded by acknowledging the proceeds from the sale and interest earnings in the local government account.

- 😀 Proper documentation of all financing transactions ensures transparency and accountability in local government financial management.

- 😀 Investment accounting tracks, measures, evaluates, and reports on both short-term and long-term investments to provide relevant information for investment decision-making.

- 😀 Liabilities in accounting refer to debts or financial obligations the government must pay in the future, including short-term liabilities like accounts payable and taxes, and long-term obligations like bank loans and bonds.

Q & A

What is the definition of accounting for financing in local government?

-Accounting for financing refers to the process of recording transactions related to the receipt and expenditure of financing in the local government's accounting journal. This includes both the income and outgoings of government financing such as loans, bond sales, and repayments.

What does the term 'Silpa' refer to in the context of local government financing?

-Silpa stands for 'Sisa Lebih Perhitungan Anggaran,' which refers to the surplus from budget calculations. This surplus is recorded as part of the financing receipt in local government accounting.

What is the role of government bonds in local government financing?

-Government bonds are a form of financing where the local government sells bonds to raise funds. The receipt of funds from these bond sales is recorded as a financing receipt in the accounting journal.

How are investment expenditures recorded in the financial accounting journal?

-Investment expenditures are recorded by debiting the long-term investment account and crediting the cash account in the local government's financial accounting journal.

What are the different methods used to recognize investments in local government accounting?

-Investments can be recognized using either the cost method or the equity method, depending on the level of ownership and influence the government holds in the investment.

How is a loan receipt recorded in the local government's accounting system?

-When a loan is received, it is recorded as a liability. In the financial journal, the receipt of cash is debited to the cash account, and the loan payable to the central government is credited.

What is the purpose of recording the sale of bonds or loans in local government finance?

-The purpose is to ensure that all financial transactions involving external borrowings or investments are accurately reflected in the local government's accounting system, ensuring transparency and accountability.

How is the receipt of dividends from investments recorded?

-When dividends are received from investments, they are recorded as other receivables in the financial journal. The corresponding credit is made to revenue from investment management.

What is the difference between short-term and long-term investments in local government accounting?

-Short-term investments are intended for temporary cash management and are easily liquidated, while long-term investments involve substantial financial commitments and are held for extended periods to generate future returns or support long-term projects.

Why is it important for local governments to properly record financing transactions?

-Accurate recording ensures transparency, accountability, and compliance with applicable regulations. It allows local governments to manage their financial resources effectively and ensures proper oversight of public funds.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade Now

5.0 / 5 (0 votes)