Perilaku Maksimisasi Profit oleh Perusahaan serta Pilihan Jangka Pendek dan Panjang (Part 41)

Summary

TLDRThis video explains the behavior of producers in a perfectly competitive market, focusing on profit maximization. It covers the production process, factors influencing decisions, and how firms balance output, technology, and costs. Key concepts like total revenue, total cost (accounting vs. economic costs), and the difference between short-term and long-term production decisions are discussed. The script highlights the importance of minimizing costs and the role of market conditions in determining profitability. The goal is to understand how firms can optimize production for maximum profit in the context of perfect competition.

Takeaways

- 😀 Producers aim to maximize profit by considering both costs and revenues, focusing on how to find profit within given conditions, rather than achieving maximum profit immediately.

- 😀 In microeconomics, three main areas are studied: consumer behavior, producer behavior, and market dynamics, with a particular emphasis on how producers operate.

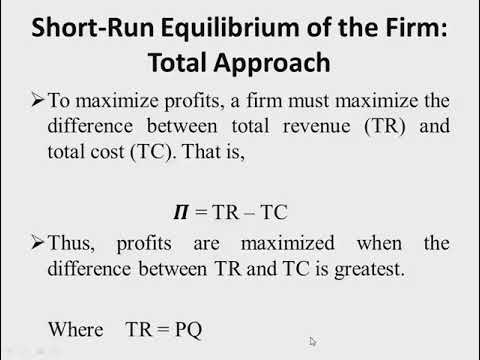

- 😀 Profit is calculated as the difference between total revenue and total cost, and revenue is derived from multiplying price by quantity sold.

- 😀 Total cost includes both explicit (out-of-pocket) costs and implicit (opportunity) costs, which are crucial for calculating economic profit.

- 😀 Economic profit differs from accounting profit by considering opportunity costs alongside explicit costs.

- 😀 Short-run production involves fixed factors, meaning the scale of production cannot be increased, and firms cannot enter or exit the industry.

- 😀 In the long run, firms have the flexibility to adjust all production factors, enter or exit the market, and make strategic decisions about expansion.

- 😀 The distinction between short-run and long-run production is based on whether production factors can be varied, not just the time frame.

- 😀 The optimal method of production is focused on minimizing costs for a given output level, which ensures efficient operations and helps maximize profit.

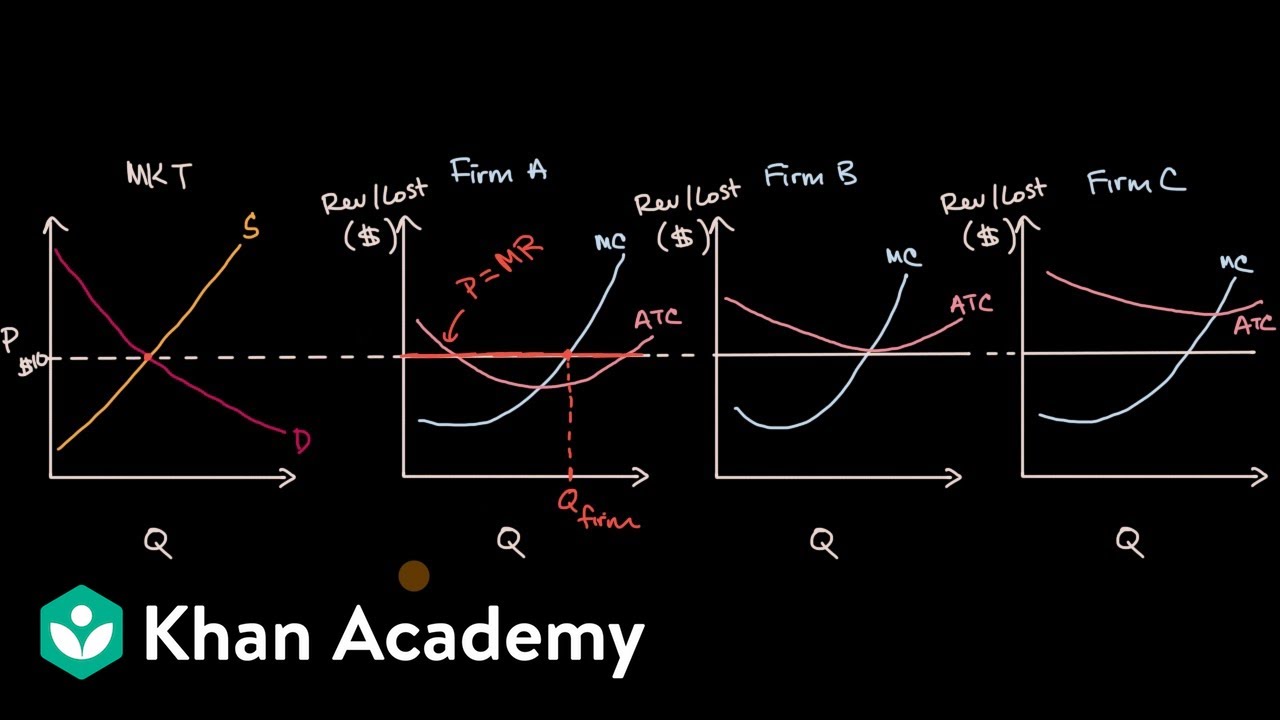

- 😀 In a perfectly competitive market, firms must accept the market price as given and cannot influence it, making revenue dependent on demand and the price level.

Q & A

What is the main focus of the lecture?

-The lecture focuses on the behavior of profit-maximizing producers, particularly in the context of kefir production, and discusses how firms maximize profits under given conditions, rather than aiming for maximum profit itself.

What are the three main branches of microeconomics mentioned in the lecture?

-The three main branches of microeconomics discussed are consumer behavior, producer behavior, and market analysis.

What is the primary goal of a producer according to the lecture?

-The primary goal of a producer is to maximize profit, which can be achieved by adjusting the level of output, production methods, and input use.

How is total revenue calculated?

-Total revenue is calculated by multiplying the price of the product (P) by the quantity sold (Q), so the formula is: Total Revenue = Price × Quantity.

What is the difference between accounting cost and economic cost?

-Accounting cost includes only explicit, out-of-pocket costs, while economic cost includes both accounting costs and opportunity costs (the cost of forgoing the next best alternative).

Why is opportunity cost important in the production process?

-Opportunity cost represents the potential benefits a firm sacrifices when choosing one production method over another, and it is a crucial component in determining the economic cost of production.

What distinguishes the short-run from the long-run in production?

-In the short run, some factors of production, like capital, are fixed, meaning a firm cannot expand or exit the industry. In the long run, all factors are variable, and firms can adjust their scale of production or enter/exit the market freely.

How does fixed capital impact production in the short run?

-In the short run, fixed capital means that the firm cannot change the scale of production beyond a certain limit, as capital remains unchanged, and it affects decisions on labor and other variable inputs.

What is the 'optimal method of production' as explained in the lecture?

-The optimal method of production is the one that minimizes the cost of producing a given level of output. This is achieved through efficient input allocation and selecting the best production technology.

How does the market condition of perfect competition affect a firm's pricing decisions?

-In perfect competition, firms are price takers and cannot control the price of their products. They can only influence their total revenue by adjusting the quantity produced, while focusing on minimizing production costs to maximize profit.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Microeconomics Unit 3 COMPLETE Summary - Production & Perfect Competition

Market Structure Part 1: Introduction

Ekonomi Mikro - Struktur Pasar Lainnya

Economic profit for firms in perfectly competitive markets | Microeconomics | Khan Academy

Perfect Competition- Microeconomics 3.7

Long run supply curve in constant cost perfectly competitive markets | Microeconomics | Khan Academy

5.0 / 5 (0 votes)