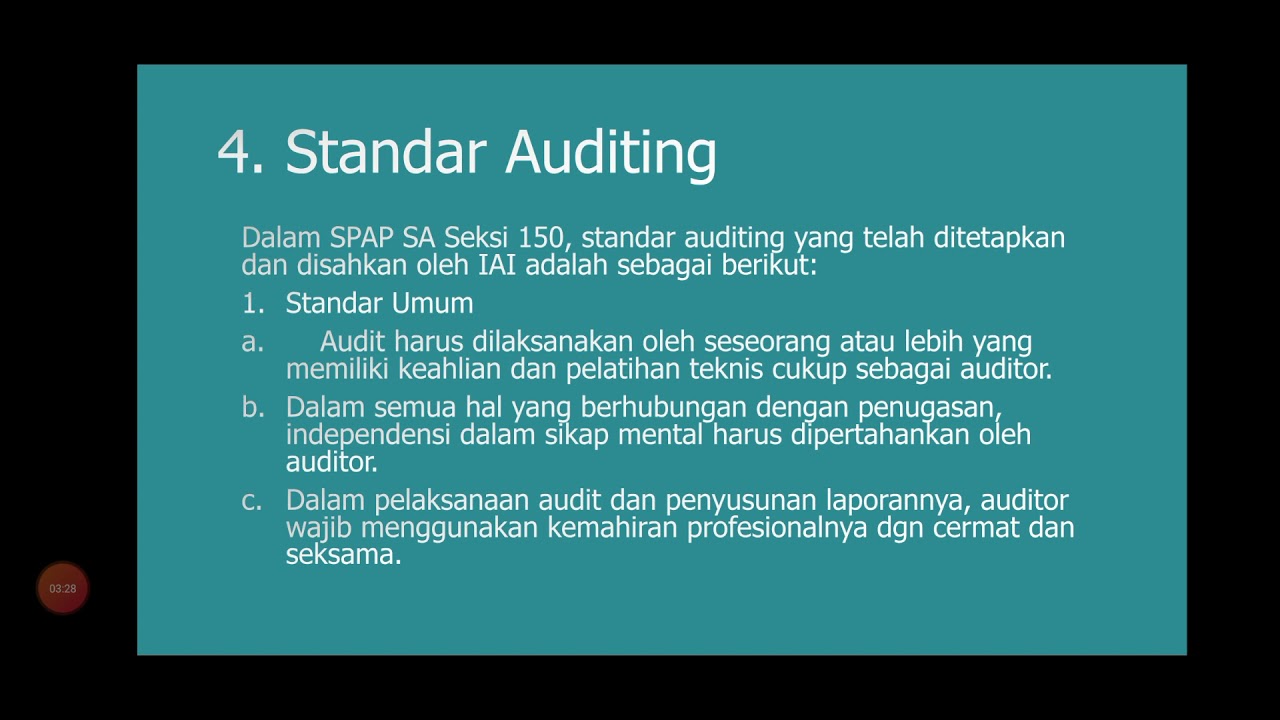

Tanggungjawab auditor, asersi dan tujuan audit

Summary

TLDRThis video transcript focuses on the responsibilities of auditors and management in financial reporting and auditing. It explains key concepts such as 'sufficient assurance' (keyakinan memadai), emphasizing the auditor's role in confirming that financial statements are free from material misstatements. The transcript also discusses various audit procedures, including assessing transactions, evaluating management assertions, and the importance of maintaining professional skepticism. Additionally, the script covers the relationship between different financial cycles, such as sales and acquisitions, and how auditors must ensure these transactions are recorded accurately. Overall, the content serves as a comprehensive guide to auditing standards and responsibilities.

Takeaways

- 😀 The script emphasizes the auditor's responsibility to obtain reasonable assurance that financial statements are free from material misstatement, whether due to error or fraud.

- 😀 The auditor's primary task is to assess whether financial statements accurately represent the company's financial position and performance according to auditing standards.

- 😀 Material misstatements refer to errors or omissions that could affect the decisions of users relying on the financial statements.

- 😀 There is a clear distinction between errors (unintentional) and fraud (intentional) in financial misstatements, and auditors must be vigilant about both.

- 😀 The concept of 'reasonable assurance' means that the auditor is confident that the financial statements are free from material misstatements, but the audit cannot guarantee absolute correctness.

- 😀 Management is responsible for ensuring the accuracy of financial statements and must provide auditors with all relevant information necessary for the audit process.

- 😀 Auditors are expected to maintain professional skepticism and not simply trust the information provided by the management, especially when it comes to financial statements.

- 😀 The script explains the importance of transaction cycles (e.g., sales, acquisition, payments) and their impact on financial statements, which auditors must carefully evaluate during an audit.

- 😀 The auditing process includes verifying the existence and accuracy of transactions, ensuring that all recorded transactions are complete and properly classified.

- 😀 The final goal of the audit is to provide assurance that the financial statements are prepared in accordance with applicable accounting principles and present an accurate picture of the company's financial status.

Q & A

What are the two main responsibilities of an auditor according to the script?

-The two main responsibilities of an auditor are: 1) To obtain reasonable assurance that the financial statements are free from material misstatement, whether caused by error or fraud. 2) To report on the financial statements in accordance with the auditing standards based on the auditor's findings.

What does 'reasonable assurance' mean in the context of an audit?

-'Reasonable assurance' refers to the level of confidence the auditor has that the financial statements are free from material misstatement. It is not an absolute guarantee but a high level of assurance that is considered acceptable in the auditing process.

How does the script define material misstatement in financial statements?

-Material misstatement refers to errors or omissions in financial statements that could influence the decision-making of users of those statements. The amount of misstatement that is considered material is subject to professional judgment.

What is the difference between fraud and error as explained in the transcript?

-Fraud involves intentional actions to deceive or misrepresent, while error refers to unintentional mistakes or omissions in the financial statements.

What role does management play in financial reporting?

-Management is responsible for preparing and presenting the financial statements in accordance with the applicable financial reporting framework. They must ensure that the statements are complete, accurate, and comply with relevant standards.

What does the auditor need to obtain from management to conduct an effective audit?

-The auditor needs unrestricted access to all relevant information within the organization, including documents, notes, and any other material that might be necessary to form an opinion on the financial statements.

What is the concept of professional skepticism, and why is it important in auditing?

-Professional skepticism refers to an attitude that includes a questioning mind and a critical assessment of audit evidence. It is essential because it helps auditors remain objective and ensure that they do not accept statements or evidence without proper scrutiny.

What are the typical transaction cycles that auditors focus on during an audit?

-Auditors typically focus on the following transaction cycles: sales and receivables, purchasing and payments, payroll, and cash flow. These cycles help identify areas where misstatements or fraud might occur in financial reporting.

How does the auditor assess the correctness of recorded transactions in financial statements?

-The auditor assesses the correctness of recorded transactions by verifying whether the transactions have been recorded accurately in the proper period, whether they are classified correctly, and whether they match supporting documentation such as invoices, contracts, or receipts.

What does the auditor need to ensure about the financial statements in relation to the accounting framework?

-The auditor needs to ensure that the financial statements comply with the relevant accounting framework and that the accounting policies applied are consistent and appropriate for the organization’s circumstances.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade Now

5.0 / 5 (0 votes)