TAX PLANNING! Strategi Memecah Badan Usaha Untuk Mengurangi Beban Pajak Yang Harus Dibayar

Summary

TLDRIn this video, the presenter discusses legal tax planning strategies through the division of business entities, aimed at reducing tax liabilities for entrepreneurs with annual revenues exceeding 4.8 million. Emphasizing the importance of compliance, the speaker outlines key considerations before splitting a business, such as revenue thresholds, legal requirements, and the implications of managing multiple entities. The video aims to educate viewers on effective tax management while avoiding pitfalls, ultimately promoting a more informed approach to business finance.

Takeaways

- 😀 Understanding legal tax planning is essential for optimizing tax expenses.

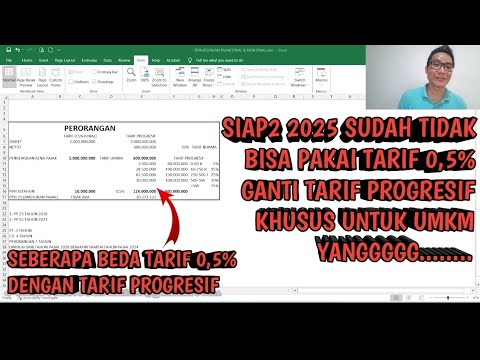

- 💰 Businesses with an annual revenue above 4.8 billion IDR face higher tax rates, potentially reaching 30%.

- 📊 Utilizing UMKM (micro, small, and medium enterprises) tax benefits can significantly reduce tax liability to just 0.5% for qualifying businesses.

- 📝 Before splitting a business entity, consider your annual revenue and whether it justifies the administrative burden.

- ⚖️ Legal tax planning should prioritize compliance to avoid stress and ensure peace of mind.

- 📦 Each split entity must handle its own transactions and inventory separately to maintain compliance.

- 🏦 Separate bank accounts for each business entity are critical; avoid using personal accounts for business transactions.

- 🔍 Evaluate your suppliers and their ability to issue tax invoices when considering splitting your business.

- 💡 Seek professional guidance to ensure your tax planning strategies are both legal and effective.

- 🔔 Educate yourself about tax obligations to prevent misunderstandings and ensure proper compliance.

Q & A

What is the main topic discussed in the video?

-The video focuses on legal tax planning through the splitting of business entities to optimize tax savings.

Why is it important to split a business entity?

-Splitting a business can help lower tax rates and reduce the overall tax burden, especially for businesses with high revenues.

What is the tax rate for UMKM if the omzet is below 4.8 billion?

-For UMKM with an omzet below 4.8 billion, the tax rate can be as low as 0.5%.

What should be considered before splitting a business?

-Key considerations include the current omzet, administrative implications, supplier capabilities for invoicing, and whether the split is financially beneficial.

What are the steps to take when splitting a business?

-Steps include establishing a separate legal entity, ensuring all transactions are separate, maintaining distinct inventory, and using separate bank accounts.

How can a business ensure compliance after splitting?

-A business must maintain proper documentation, ensure transactions and inventories are kept separate, and adhere to legal requirements for each entity.

What is the potential future change regarding the omzet threshold?

-There is speculation that the omzet threshold for UMKM may be lowered, potentially affecting tax rates.

What common mistake do entrepreneurs make regarding bank accounts?

-Many entrepreneurs mistakenly use their personal bank accounts for business transactions, which can lead to legal issues.

How does proper tax planning alleviate stress for business owners?

-Legal and effective tax planning allows business owners to focus on growth and operations without the constant worry of tax liabilities.

Where can viewers seek additional information or clarification?

-Viewers are encouraged to comment on the video or follow the presenter on social media for quick responses to their questions.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

5.0 / 5 (0 votes)