How To Build Wealth With $0 - The Easy Way

Summary

TLDRThe video emphasizes the challenges faced by the financially disadvantaged in building wealth and offers unconventional advice for wealth accumulation. It suggests avoiding traditional financial tips and instead listening to successful individuals. The speaker recommends choosing careers with income potential beyond hourly wages, such as sales, and emphasizes the importance of investing early and consistently, even with small amounts. The video also encourages creating multiple income streams and provides a step-by-step guide to potentially reaching $500,000 in wealth within a decade, highlighting the importance of avoiding lifestyle inflation and investing additional income.

Takeaways

- 💼 The video emphasizes the challenge of wealth-building for those without a financial safety net and suggests that traditional advice is often insufficient.

- 💰 It highlights that only 30% of the poorest American families have savings accounts, indicating a significant portion of the population is financially vulnerable.

- 🏦 The speaker argues against common financial misconceptions like avoiding credit cards or loans, and instead encourages learning from successful individuals.

- 🚀 The video suggests pursuing careers or businesses with income potential not capped by the number of hours worked, such as sales or entrepreneurship.

- 💹 It stresses the importance of investing early and often, using the power of compound interest to grow wealth over time.

- 💲 The speaker recommends opening a Roth IRA for tax-free growth and highlights the benefits of long-term investing for significant financial gains.

- 🔄 The video encourages creating multiple income streams, citing IRS research that shows a correlation between the number of income streams and higher earnings.

- 🏠 Real estate is presented as a powerful wealth-building tool, offering tax advantages and potential for both rental and capital gains income.

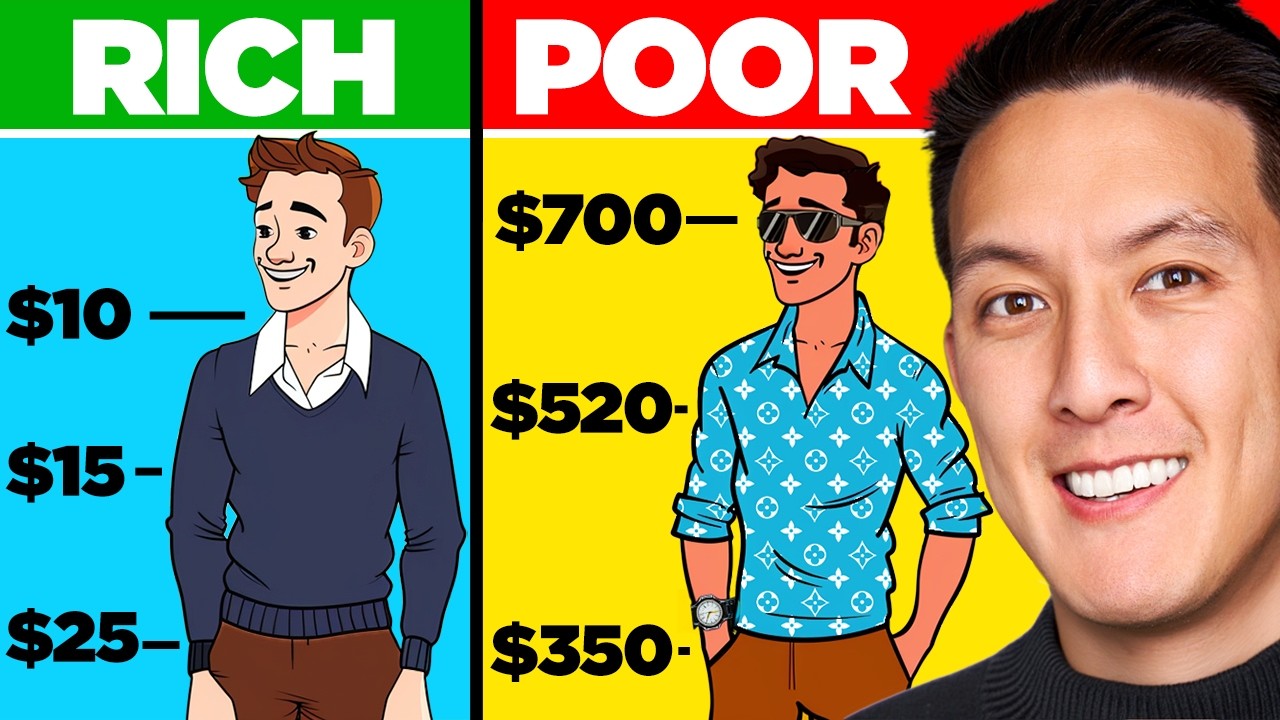

- ⏰ The script advises against lifestyle inflation, which can erode savings, and instead suggests maintaining expenses while investing additional income from raises or side hustles.

- 🔑 The key to reaching financial goals is dedication, sacrifice, and strategic financial planning, which can potentially transform one's financial future within a decade.

Q & A

What is the main challenge faced by the poorest American families according to the script?

-The main challenge is that just 30% of the poorest American families have a savings account, and many working Americans still can't afford basic necessities like food and rent.

What percentage of Americans are said to be living paycheck to paycheck in the script?

-54% of Americans are said to be living paycheck to paycheck.

What is the average amount it would take for middle-class Americans to feel financially secure, as mentioned in the script?

-The average amount it would take for middle-class Americans to feel financially secure is $500,000.

What is the advice given for someone starting from nothing to build wealth, according to the script?

-The advice includes not following generic financial advice, being cautious about who you listen to, choosing a career or business not dependent on hours worked, and investing everything immediately.

Why are traditional jobs not recommended for building wealth quickly in the script?

-Traditional jobs are not recommended because they often pay hourly and have a ceiling on income based on the number of hours one can work, which limits the potential for wealth accumulation.

What career is suggested as a stepping stone to making more money in the script?

-Sales is suggested as a stepping stone to making more money because it can provide funding for other ventures and teaches important skills like time management and customer service.

What is the significance of investing early according to the script?

-Investing early is significant because it allows the money more time to grow. For example, $1 invested at 20 with a 7% return will be worth $21 by 65, whereas waiting until 30 will only yield $10.68 by 65.

What is a Roth IRA and why is it recommended in the script?

-A Roth IRA is a retirement account where contributions are made with after-tax dollars, and the profits are tax-free after the age of 59 and a half. It is recommended because it allows for tax-free growth and provides an additional avenue for investment.

How does the script suggest creating multiple sources of income can help build wealth?

-The script suggests that the more income streams one has, the more income they tend to make. It cites a study where 65% of millionaires have three or more sources of income, indicating diversification is key to wealth building.

What is the importance of avoiding lifestyle inflation when trying to build wealth according to the script?

-Lifestyle inflation occurs when one increases their spending as their income increases, which can prevent wealth accumulation. The script emphasizes maintaining the same expenses and investing the additional income to continue building wealth.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

15 Reasons Why The Rich Are Getting Richer

7 Major Differences Between Rich and Poor People

المُخبر الاقتصادي+ | ما الأخطاء التي قد تجعلك فقيراً للأبد؟ وكيف يخسر الناس أموالهم؟!

17 Money Secrets To Make Your First $1,000,000

The Most Vile Financial Influencer

How America Created Its Shameful Wealth Gap | Robert Reich

5.0 / 5 (0 votes)