Komponen pengendalian internal COSO

Summary

TLDRThe video script discusses the five components of internal control as outlined by COSO, which are further elaborated into 17 principles. The first component, the control environment, includes policies and procedures that reflect the management's attitude towards internal control, emphasizing integrity and ethics. The second component involves the participation of the board of directors and audit committees in overseeing internal control performance. The third component, organizational structure, deals with the division of authority and responsibility within the company. The fourth component is about commitment to competence, ensuring that only competent individuals are employed and retained. The fifth component, risk assessment, involves identifying and managing risks that could hinder the company's objectives. The video also covers the importance of information and communication within internal control, ensuring that all members of the company receive accurate and relevant information. Lastly, the script touches on the monitoring of internal control systems to ensure they are functioning as expected and are in line with the company's goals.

Takeaways

- 📚 The script discusses the five components of internal control according to COSO, which are further elaborated into 17 principles.

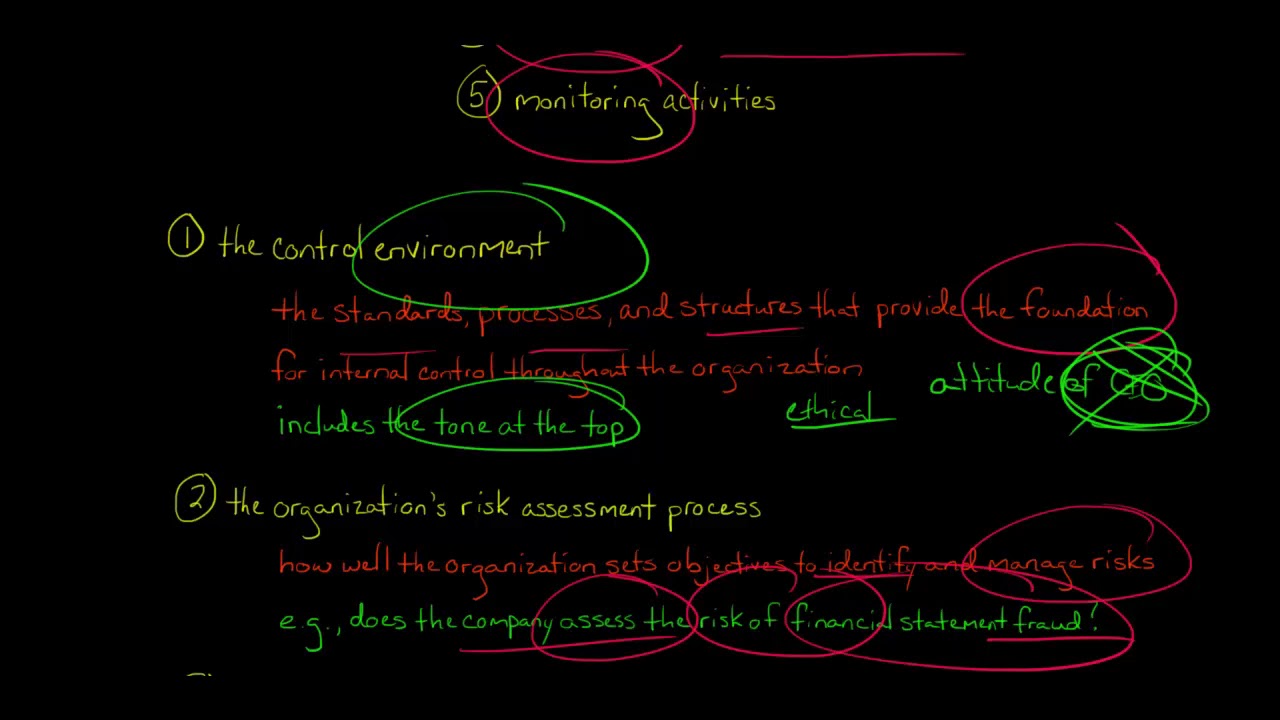

- 🏢 The first component is the 'Control Environment', which includes policies and procedures reflecting the management's attitude towards internal control within a company.

- 👨💼 Integrity and ethics are the first principles under the control environment, demonstrated by top management through policies and actions emphasizing the importance of internal control.

- 👥 The second principle involves the participation of the board of directors and audit committee, which should show independence in overseeing the development of internal control performance.

- 🏛 The third principle is 'Organizational Structure', which includes the division of authority, responsibility, and tasks within the company to prevent concentration of power.

- 💼 The fourth principle is 'Commitment to Competence', where the company must demonstrate commitment by hiring and retaining competent individuals based on merit.

- 🔍 The second component, 'Risk Assessment', involves identifying potential risks that could hinder the company's objectives and managing these risks effectively.

- 📉 The first principle under risk assessment is having clear objectives for identifying risks, understanding the likelihood and impact of potential risks on the company's goals.

- 🛡 The third component, 'Control Activities', refers to policies and procedures established by management to achieve the company's objectives and mitigate risks to an acceptable level.

- 🔄 The fourth component, 'Information and Communication', is crucial for connecting top management to the lowest level, ensuring accurate and timely information sharing to maintain accountability.

- 👁️ The last component, 'Monitoring', involves ongoing monitoring of activities and periodic evaluations to ensure internal controls are functioning as expected and to identify areas for improvement.

Q & A

What are the five components of internal control according to the script?

-The five components of internal control are the control environment, risk assessment, control activities, information and communication, and monitoring.

What is the significance of the control environment in internal control?

-The control environment sets the tone for the entire organization, influencing the importance and priority given to internal control. It includes the integrity and ethics of top management and the commitment to competence of all personnel.

How does the participation of the board of directors and audit committee relate to internal control?

-The board of directors and audit committee should demonstrate independence in overseeing the development and performance of internal control. Their actions reflect the company's commitment to internal control.

What is the role of organizational structure in internal control?

-The organizational structure includes the division of authority and responsibility, which is crucial for separating duties to prevent concentration of power and to ensure accountability.

Why is the commitment to competence important in a company's internal control?

-Commitment to competence ensures that only qualified individuals are hired and retained, which is essential for the effectiveness of internal control. It starts with HR during recruitment and involves maintaining competent employees within the company.

How should accountability be managed within a company?

-Accountability should be clear, flowing from the bottom up and from the top down, ensuring that all members of the organization have a sense of responsibility and are accountable for their actions.

What is risk assessment in the context of internal control?

-Risk assessment involves identifying and analyzing risks that could jeopardize the achievement of the company's objectives. It is about understanding the likelihood and impact of potential events on the entity's ability to achieve its objectives.

What are control activities within internal control?

-Control activities are the policies and procedures that help ensure that the company's objectives are achieved. They are actions taken by management to mitigate risks identified during risk assessment to an acceptable level.

How does information and communication relate to internal control?

-Information and communication is the means by which all members of an organization share and receive information necessary for carrying out their responsibilities. It is crucial for initiating, recording, processing, and reporting transactions and events for ensuring accountability.

What is the purpose of monitoring activities in internal control?

-Monitoring activities are used to assess the quality of internal control system performance over time. It involves ongoing monitoring as well as periodic evaluation to ensure that the internal control system is functioning as intended.

How should a company handle changes that could potentially introduce new risks?

-Companies should continuously monitor for changes that could affect risks and the effectiveness of controls. When changes occur, the company must assess the impact on risk and control, and make necessary adjustments to maintain effective internal control.

What are the principles that should guide the sharing of information within and outside the company?

-Information should be relevant, high-quality, and timely. Internally, information should be communicated to ensure all members understand their roles and responsibilities. Externally, information should be shared selectively with parties outside the company who have a legitimate interest in the company's internal control, such as banks or regulatory bodies.

Outlines

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードMindmap

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードKeywords

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードHighlights

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードTranscripts

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレード

5.0 / 5 (0 votes)