Classification of Individual Taxpayer (Residency)

Summary

TLDRIn this educational video, Leroy discusses the classification of taxpayers based on residency for income tax purposes in the Philippines. He explains the four categories: resident citizens, non-resident citizens, resident aliens, and non-resident aliens. Each classification has specific tax implications, with resident citizens taxed on worldwide income and non-resident citizens on income from the Philippines only. The video emphasizes the importance of establishing residency status through documents like visas and contracts, which can affect tax obligations and potentially estate taxes.

Takeaways

- 📚 The video discusses the classification of taxpayers based on residency for income tax purposes.

- 🏠 Resident citizens are those who reside within the Philippines and are defined by the 1987 Constitution.

- 🌐 Non-resident citizens are those who establish physical presence abroad with the intention to reside there.

- 🏢 Resident aliens are individuals who live in the Philippines but are not citizens.

- 🚀 Non-resident aliens are individuals who do not reside in the Philippines and are not citizens.

- 🔍 Non-resident aliens are further divided into those engaged in trade or business and those not engaged, based on their stay duration in the Philippines.

- 💼 Taxation for resident citizens includes income from both within and outside the Philippines.

- 🌍 Non-resident citizens are taxed only on income derived from within the Philippines.

- 🏦 Alien individuals, whether resident or not, are taxed only on income derived within the Philippines.

- 📑 Taxpayers' intentions regarding their stay are determined by submitting documents like visas and contracts to the Bureau of Internal Revenue (BIR).

- 👍 The video emphasizes the importance of understanding these classifications for both income and estate tax implications.

Q & A

What are the four classifications of taxpayers based on residency mentioned in the video?

-The four classifications of taxpayers based on residency are: Resident Citizen, Non-Resident Citizen, Resident Alien, and Non-Resident Alien.

According to the 1987 Philippine Constitution, who are considered citizens of the Philippines?

-According to the 1987 Constitution, citizens of the Philippines include those who were citizens at the time of the constitution's adoption, those whose fathers or mothers are citizens, those born before January 17, 1973 of Filipino mothers who elect Philippine citizenship upon reaching the age of majority, and those who are naturalized in accordance with the law.

What is the definition of a Non-Resident Citizen as per the Philippine Tax Code?

-A Non-Resident Citizen is defined as a citizen of the Philippines who establishes to the satisfaction of the Commissioner the fact of his physical presence abroad with the definite intention to reside therein.

What are the conditions for a citizen to be considered a Non-Resident Citizen for tax purposes?

-A citizen can be considered a Non-Resident Citizen for tax purposes if they leave the Philippines during the taxable year to reside abroad either as an immigrant or for employment on a permanent basis, work and derive income from abroad requiring them to be physically present abroad most of the time, or have been previously considered a Non-Resident Citizen and arrive in the Philippines to reside permanently.

What is the difference between a Resident Alien and a Non-Resident Alien?

-A Resident Alien is an individual who resides within the Philippines but is not a citizen thereof. A Non-Resident Alien is an individual whose residency is not in the Philippines and is not a citizen thereof.

How are Non-Resident Aliens classified for tax purposes in the Philippines?

-Non-Resident Aliens are classified based on their engagement in trade or business and their aggregate stay in the Philippines. If their stay is more than 180 days, they are engaged in trade or business. If their stay is 180 days or less, they are not engaged in trade or business.

How is the tax liability determined for Resident Citizens and Non-Resident Citizens?

-Resident Citizens are taxed on income derived within and outside of the Philippines, whereas Non-Resident Citizens are taxed on income derived within the Philippines only.

What is the tax liability for Alien individuals, whether Resident or Non-Resident, in the Philippines?

-Alien individuals, whether Resident or Non-Resident, are only taxed on income derived within the Philippines.

Why is the intention of the taxpayer with regards to the nature of their stay important for tax purposes?

-The intention of the taxpayer regarding the nature of their stay is important because it determines their residency status, which in turn affects how they are taxed and which tax regulations apply to them.

What documents can be submitted to the Bureau of Internal Revenue (BIR) to demonstrate the intention of residency?

-Documents such as visas, contracts, and others that show the intention of residency can be submitted to the BIR. For example, a Resident Citizen with a tourist visa would typically be classified as a Resident Citizen, while one with a working visa for three years might be reclassified as a Non-Resident Citizen upon departure.

How does understanding the classification of taxpayers based on residency relate to estate taxes?

-Understanding the classification of taxpayers based on residency is important for estate taxes as it determines the tax liabilities and regulations that apply to the estate of a deceased individual, especially concerning their residency status and the location of their assets.

Outlines

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードMindmap

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードKeywords

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードHighlights

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードTranscripts

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレード関連動画をさらに表示

Residence Status and Scope of Total Income,L5 Samarthya IAS & JUDICIARY #incometax #taxation #income

Situs of Taxation + Quiz

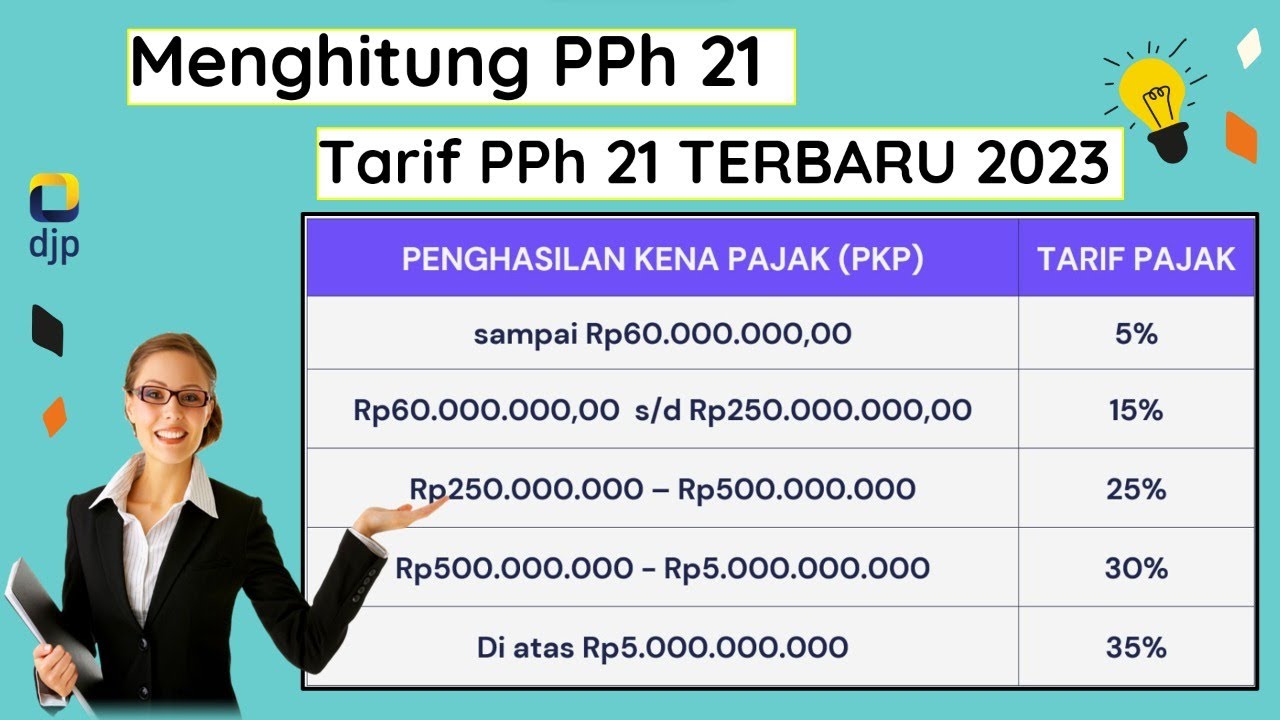

Menghitung Pajak Penghasilan PPh 21 terbaru tahun 2023 #pph21 #pajakpenghasilan #pajak

Menghitung Pajak Penghasilan Berdasarkan UU Nomor 7 Tahun 2021 (Part 1)

How to become an NRI. And pay 0% tax, legally | Akshat Shrivastava

KPMG PH Insights: EOPT Series Episode 1 (Overview of the EOPT Act)

5.0 / 5 (0 votes)