#MateriKuliahAKS Standar Audit (SPAP) Terbaru

Summary

TLDRThis video discusses the recent changes to auditing standards issued by the Indonesian Institute of Public Accountants (IAPI). The speaker outlines the shift from the previous 10 auditing standards to a more structured and updated set of standards, categorized into general standards, fieldwork standards, and reporting standards. Key aspects covered include risk assessment, audit evidence, the use of third-party work, and the formulation of audit opinions. Additionally, the video touches on the new professional standards and ethical codes, emphasizing the importance of applying the correct standards during the audit process to ensure accurate financial reporting.

Takeaways

- 😀 The Indonesian Institute of Public Accountants (IAPI) has updated auditing standards, transitioning from 10 previous standards to a new structure based on IMX6, effective from 2011.

- 😀 The new standards categorize auditing practices into two major segments: 'audit of historical financial statements' and 'examination of prospective financial statements,' with specific guidelines for each.

- 😀 Standards for assurance engagements now include reviews and consultations, alongside audits, with a shift to a structured, risk-based approach as outlined in the updated guidelines.

- 😀 The new audit standards (SA 200-800) emphasize principles such as auditor responsibility, risk assessment, evidence gathering, and reporting, with clear definitions for each.

- 😀 Evidence collection is key in the auditing process, requiring auditors to gather sufficient and competent evidence to form a conclusion on financial statements.

- 😀 Auditors now follow a more streamlined process, assessing risks and response strategies, including both the evaluation of internal controls and substantive testing of transactions.

- 😀 Standard SA 600-620 covers the use of external work, including auditors collaborating with external professionals or using internal audit reports as part of the audit process.

- 😀 The new reporting standards (SA 700-750) guide auditors in forming an opinion and addressing any modifications, including the necessity of adding special paragraphs to highlight specific matters in the audit report.

- 😀 The audit approach now places a significant focus on the auditor’s professional judgment and skepticism, as well as the identification and evaluation of risks related to material misstatements.

- 😀 Auditors follow a risk-based approach in their evaluations, categorizing assertions as high, medium, or low risk, which influences the type of audit opinion provided, such as 'unmodified' or 'modified' opinions based on findings.

Q & A

What are the key changes in the auditing standards in Indonesia?

-The key changes involve the replacement of the previous 10 standards with a more structured framework consisting of six main components: principles and auditor responsibilities, risk assessment and response, audit evidence, use of work by others, audit conclusions and reporting, and special areas.

What are the three main categories of the old auditing standards?

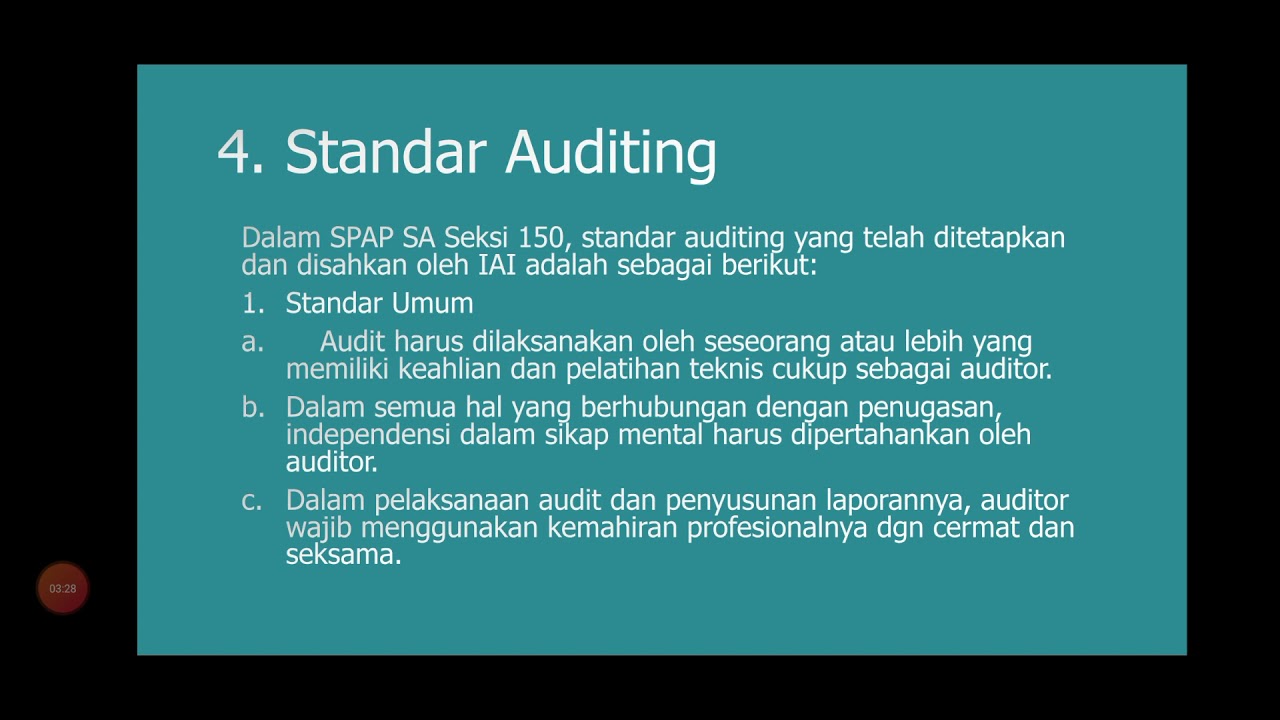

-The old auditing standards were divided into three categories: general standards, fieldwork standards, and reporting standards.

How has the structure of the auditing standards changed under the new system?

-The new structure consolidates the previous 10 standards into six main components: auditor responsibilities, risk assessment, audit evidence, use of work by others, audit conclusions, and reporting, with special areas reserved for specific audit scenarios.

What does SA 200–265 cover in the updated auditing standards?

-SA 200–265 cover the general principles and auditor responsibilities, which include the auditor's role, ethical conduct, and procedures for planning the audit with professional skepticism.

What is the purpose of the risk assessment process in auditing (SA 300–450)?

-The purpose of the risk assessment process is to identify and assess the risks of material misstatement in financial statements and to design audit procedures to respond appropriately to these risks.

What does SA 500–580 focus on in the new standards?

-SA 500–580 focus on the collection of audit evidence. Auditors must gather sufficient and competent evidence, using techniques like confirmation from external parties and analytical procedures to ensure completeness and accuracy in financial reporting.

Why is the use of work by others (SA 600–620) important in auditing?

-The use of work by others is important because auditors may rely on internal auditors or external experts during the audit. They must evaluate the adequacy of their work to ensure it aligns with auditing standards and supports the overall audit conclusion.

What is the significance of SA 700–750 in the auditing process?

-SA 700–750 focus on audit conclusions and reporting. They guide the auditor in forming an opinion on the financial statements and reporting any modifications or additional emphasis, such as highlighting material misstatements or uncertainties.

How does the risk-based approach affect the auditing process?

-The risk-based approach requires auditors to assess the risk of material misstatements at both the financial statement level and the assertion level, tailoring audit procedures based on the identified risks. This ensures audits are more efficient and focused on high-risk areas.

What role does professional skepticism play in the updated auditing standards?

-Professional skepticism is essential in the updated standards as auditors are required to approach the audit with a questioning mind, remaining alert to the possibility of fraud or error, and critically evaluating the evidence they collect during the audit.

Outlines

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantMindmap

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantKeywords

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantHighlights

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantTranscripts

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenant

5.0 / 5 (0 votes)