Konsep Dasar Akuntansi Manajemen

Summary

TLDRThis video provides an overview of fundamental concepts in managerial accounting, emphasizing the importance of cost allocation and its impact on decision-making within a company. Key topics include cost identification, classification, and allocation methods such as direct tracing, cost drivers, and indirect cost allocation. It also highlights the role of accurate cost accounting in pricing, profitability analysis, and strategic decisions. The difference between tangible and intangible products, as well as the various cost classifications like direct materials, labor, and overhead, are also explored in detail to aid in external financial reporting and management decisions.

Takeaways

- 😀 Management accounting provides information for internal users to assist in planning and decision-making.

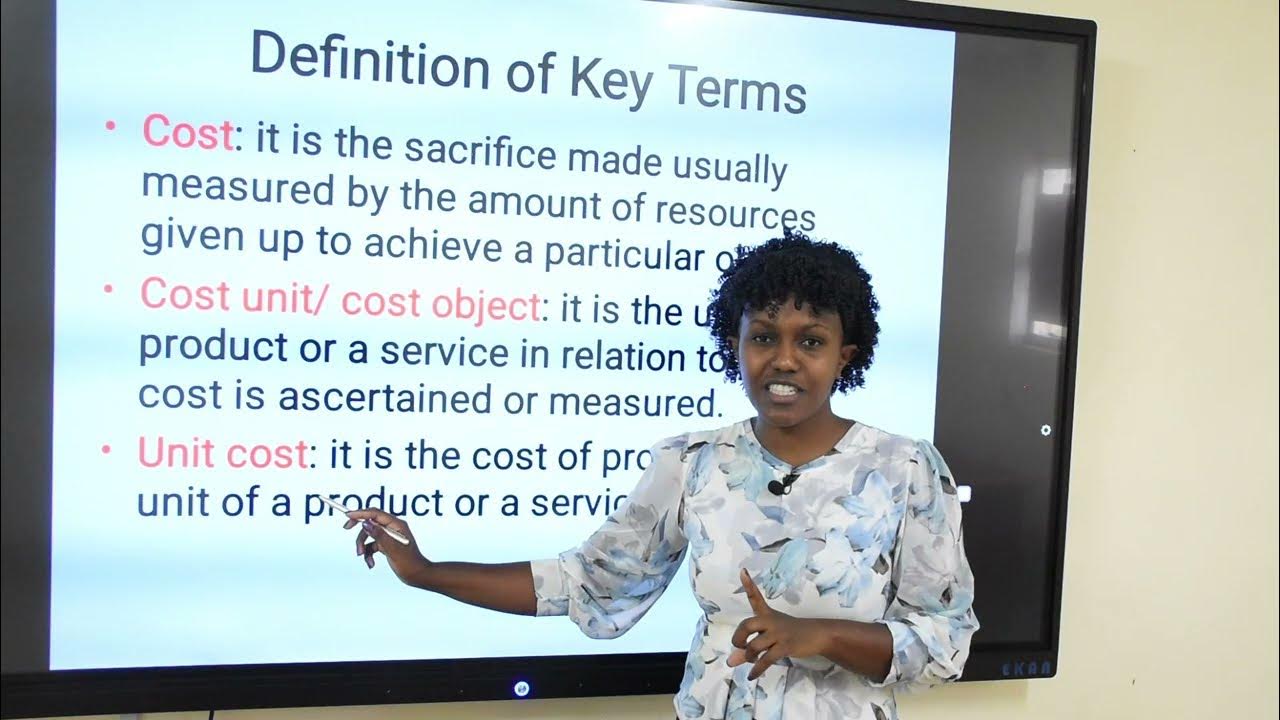

- 😀 Costs are resources sacrificed, such as cash, to obtain goods or services expected to provide current or future benefits.

- 😀 Cost objects can be anything, such as products, customers, departments, projects, or activities, that incur costs.

- 😀 Accurate cost allocation is critical; misallocation can lead to incorrect product pricing and uncompetitive market positions.

- 😀 Direct tracing, driver tracing, and allocation are the three primary methods of assigning costs to objects.

- 😀 Driver tracing uses activity drivers to assign costs based on cause-and-effect relationships, e.g., electricity cost depending on working hours.

- 😀 Allocation is used for indirect costs that cannot be traced directly or through drivers, based on assumed relationships.

- 😀 Company outputs are either tangible products (goods) or intangible products (services), each with distinct characteristics.

- 😀 Services are intangible, perishable, inseparable from the provider, and heterogeneous, making cost and quality measurement different from goods.

- 😀 Product cost information varies depending on managerial purposes, such as strategic decisions, tactical analysis, or external financial reporting.

- 😀 For external financial reporting, only production costs (direct materials, direct labor, and overhead) are included, excluding marketing or R&D costs.

- 😀 Understanding cost behavior and purpose is essential for profitability analysis, pricing, and strategic decision-making in both manufacturing and service organizations.

Q & A

What is management accounting according to Hansen and Mowen?

-Management accounting is a system that produces information for internal users within an organization. The information is used by managers to support planning, decision-making, and organizational control.

Who are the primary users of management accounting reports?

-The primary users are internal stakeholders, especially managers and management teams within a company who use the information for planning, controlling operations, and making strategic decisions.

What activities are involved in management accounting?

-Management accounting involves identifying, collecting, measuring, classifying, and reporting information that is useful for internal decision-making and planning.

What is the definition of cost in management accounting?

-Cost is defined as cash or cash-equivalent value sacrificed to obtain goods or services that are expected to provide benefits either in the present or in the future for the organization.

What is a cost object?

-A cost object is anything for which costs are measured and assigned, such as products, customers, departments, projects, or activities.

Why is accuracy in cost assignment important?

-Accurate cost assignment is crucial because inaccurate cost allocation can lead to incorrect product costs, which may result in inappropriate pricing decisions and reduced competitiveness in the market.

What is direct tracing in cost allocation?

-Direct tracing is the process of identifying and assigning costs that can be physically and directly associated with a specific cost object, such as fabric, buttons, and thread used in making a shirt.

What is driver tracing in cost allocation?

-Driver tracing uses activity drivers to assign costs to cost objects. A cost driver is a factor that causes a change in resource usage and has a cause-and-effect relationship with the cost.

Can you give an example of a cost driver?

-An example of a cost driver is working hours influencing electricity costs. The longer the working hours, the more electricity is used, increasing the electricity expense.

What is allocation in cost assignment?

-Allocation refers to assigning indirect costs to cost objects when there is no direct or clear cause-and-effect relationship. These costs are distributed based on assumed relationships.

What are the two main types of outputs produced by companies?

-Companies produce two main types of outputs: tangible products (physical goods) and intangible products (services).

What is a manufacturing organization?

-A manufacturing organization is a company that processes raw materials into semi-finished or finished physical goods.

What is a service organization?

-A service organization provides intangible services to customers, such as auditing services, banking services, or car rental services.

What are the four main characteristics of services compared to physical products?

-The four characteristics are intangibility (cannot be seen or touched before purchase), perishability (cannot be stored for future use), inseparability (production and consumption occur simultaneously), and heterogeneity (services may vary in quality and delivery).

What are the three main components of production cost used in external financial reporting?

-The three components are direct materials, direct labor, and manufacturing overhead.

What is the difference between production costs and non-production costs?

-Production costs relate directly to manufacturing a product and include materials, labor, and overhead. Non-production costs include selling expenses and administrative expenses.

Why does product cost depend on managerial objectives?

-Different managerial goals require different cost information. For example, pricing decisions, product mix decisions, profitability analysis, or financial reporting may each require different definitions of product cost.

Outlines

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenMindmap

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenKeywords

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenHighlights

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenTranscripts

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenWeitere ähnliche Videos ansehen

5.0 / 5 (0 votes)