Educational session on draft ESRS S1 Own workforce

Summary

TLDRSig Vitols presents an overview of the draft European sustainability reporting standard S1, focusing on the 'Own Workforce.' The standard is guided by the Corporate Sustainability Reporting Directive (CSRD) and emphasizes due diligence, human rights, and social factors such as equal opportunities, working conditions, and workplace safety. It mandates transparency for companies with 250+ employees, requiring disclosures on workforce impact, risks, diversity, health and safety, and pay equality. The standard also harmonizes reporting on workers across all affected stakeholder groups, including employees, non-employees, and the broader value chain, aligning with international human rights frameworks.

Takeaways

- 😀 The European sustainability reporting standard S1 focuses on workforce-related disclosures, as part of the Corporate Sustainability Reporting Directive (CSRD).

- 😀 The CSRD provides two key articles—29a and 29b—which guide the development of the S1 standard, emphasizing due diligence and reporting on social impacts.

- 😀 Article 29a requires companies to describe their due diligence processes and address adverse impacts related to their operations, particularly on their workforce.

- 😀 Article 29b mandates disclosures on various social factors, including equal treatment, working conditions, health and safety, and workers' rights to freedom of association.

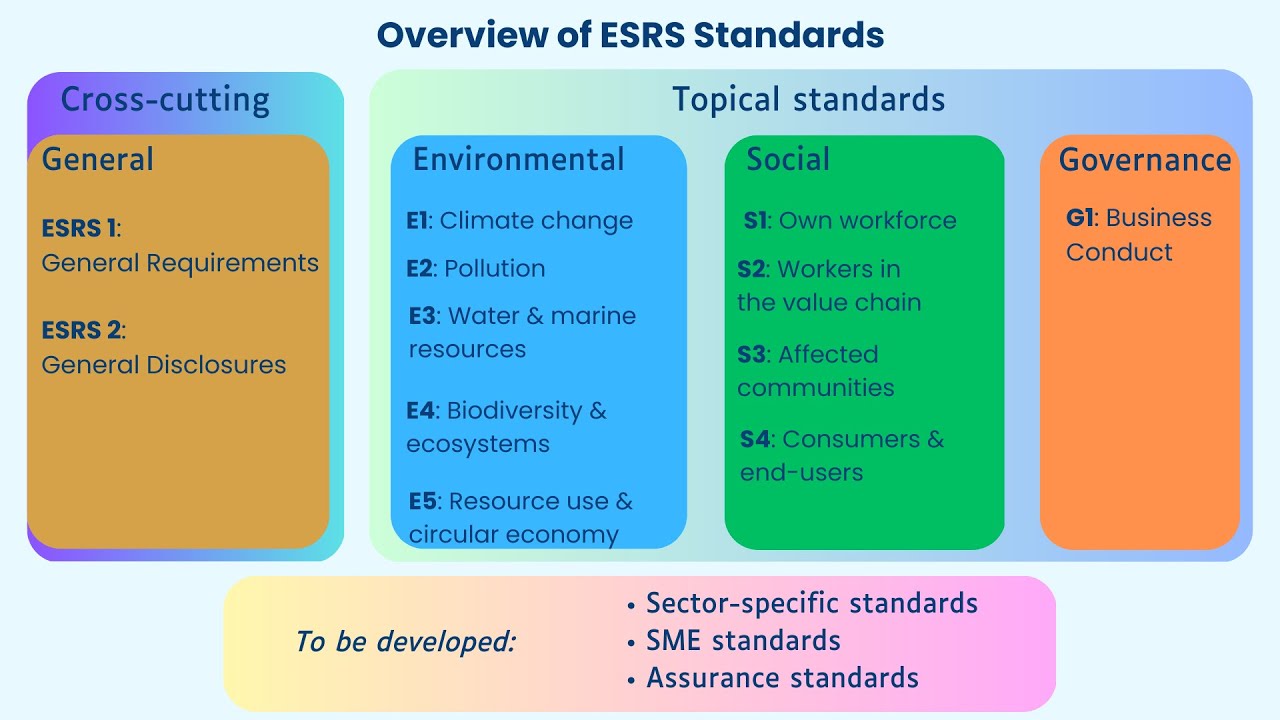

- 😀 The social pillar under CSRD consists of four distinct standards: own workforce (S1), value chain workers, affected communities, and consumers/end users.

- 😀 S1 defines the scope of workers to include both employees (those with an employment relationship) and non-employee workers (self-employed and agency workers).

- 😀 Companies with more than 250 employees are required to provide mandatory disclosures on key social factors, including gender equality, diversity, training, wages, and social dialogue.

- 😀 The S1 standard aligns with international human rights and due diligence norms defined by the UN and OECD, ensuring global consistency in reporting.

- 😀 S1's disclosure requirements cover a range of metrics and key performance indicators (KPIs), such as diversity in management, pay inequality, health and safety incidents, and workforce training hours.

- 😀 Some disclosures are subject to materiality assessments, meaning companies report only if the issue is deemed material to their operations based on a formal process.

- 😀 S1 incorporates elements from global reporting frameworks such as the Global Reporting Initiative (GRI) and the Sustainable Finance Disclosure Regulation (SFDR), ensuring harmonization with international standards.

Q & A

What is the focus of the European Sustainability Reporting Standard S1?

-The focus of S1 is on the reporting requirements for a company's 'Own Workforce,' including employees and non-employee workers such as contractors and agency workers.

Which articles of the Corporate Sustainability Reporting Directive (CSRD) are most relevant to the development of S1?

-Articles 29a and 29b of the CSRD are the most relevant. Article 29a focuses on due diligence processes aligned with international norms, while Article 29b specifies the need for reporting on social factors like equality, working conditions, and human rights.

What international frameworks guide the development of the S1 standard?

-The S1 standard is guided by international due diligence norms, particularly the UN Guiding Principles on Business and Human Rights and the OECD Guidelines on Due Diligence.

What is the structure of the social pillar in sustainability reporting?

-The social pillar is divided into four standards based on affected stakeholder groups: 1) Own Workforce (S1), 2) Workers in the value chain, 3) Affected communities, and 4) Consumers and end-users. These standards share common disclosure requirements on social matters.

What types of workers are included under S1?

-S1 covers both employees (those in a formal employment relationship) and non-employee workers, which include self-employed contractors and agency workers who are integral to the company's operations.

What are the first five disclosure requirements under S1 based on?

-The first five disclosure requirements under S1 are harmonized with other social standards and are based on international due diligence frameworks, particularly the UN and OECD guidelines, as well as the Sustainable Finance Disclosure Regulation (SFDR).

What is the purpose of materiality assessments in the context of S1 reporting?

-Materiality assessments are used to determine which social issues are most relevant to a company's operations. Disclosure requirements that are subject to materiality assessments include areas such as worker disability, training, health and safety, and pay inequality.

Which social factors must companies report under Article 29b of the CSRD?

-Under Article 29b, companies are required to report on factors like equal treatment and opportunities (including gender equality and equal pay), training and skill development, working conditions (e.g., secure employment, working time, and health and safety), social dialogue, and human rights.

How does S1 ensure transparency regarding worker engagement and social dialogue?

-S1 requires companies to disclose their policies and practices related to worker engagement, including processes for consulting workers and their representatives on social matters, collective bargaining, and mechanisms for addressing concerns raised by employees.

What specific metrics or KPIs are included in S1 reporting requirements?

-S1 includes metrics related to workforce composition (e.g., gender and age diversity), pay equality (e.g., male/female pay gap, CEO-to-median pay ratio), collective bargaining coverage, and worker participation in social dialogue. These metrics aim to provide a clear picture of a company's labor practices.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级浏览更多相关视频

PENGANTAR UMUM PROGRES ISSB: IFRS SUSTAINABILITY DISCLOSURE STANDARD-EXPOSURE DRAFT IFRS S1

Sustainability Matters Ep 2.1 - From voluntary to mandatory: understanding IFRS S1 and S2

Educational session on draft ESRS S2, S3 & S4

#ESRS Standards: Your Essential Overview

EU Finance Podcast: Episode 13 - The one about sustainability reporting

Upskilling for ESG Reporting - Learning CSRD / ESRS. How I Started.

5.0 / 5 (0 votes)