COMO ENSINEI MEU AMIGO A DOBRAR SUA RESERVA DE FORMA SIMPLES E NA PRÁTICA! COMPARTILHEI COM VOCÊ !!

Summary

TLDRIn this video, the speaker explains how to select the best investment options based on an individual's financial goals and risk tolerance. They compare different financial products, such as fixed-income investments and savings accounts, highlighting the benefits and risks of each. Using a practical example, the speaker demonstrates how an investment of R$50,000 could grow over time, and contrasts the returns of more liquid options versus longer-term investments. The video also delves into the potential of turning R$50,000 into R$1 million through long-term investments in variable income products. The speaker encourages viewers to assess their investment needs and provides advice on both short-term and long-term strategies.

Takeaways

- 😀 A fixed-income product with a guaranteed return can outperform high-liquidity options, such as savings accounts or bank products offering 100% of CDI.

- 😀 Investing in a product with a pre-determined interest rate, such as 14.95% annually, can provide a higher return over time compared to more liquid options.

- 😀 An investment of R$ 50,000 in a fixed-income product with 13.18% net return can potentially grow to R$ 94,800 over 5 years by 2030.

- 😀 High-liquidity products, like those from Nubank or Banco Inter, offer lower returns than products locked for a longer term, even if they give slightly more than 100% of CDI.

- 😀 Fixed-income products come with risks, particularly if interest rates rise higher than expected. This could result in better returns from other financial products not available at the time of initial investment.

- 😀 It's important to consider the duration of the investment. Longer-term financial products (5 years or more) may provide better returns compared to short-term liquid options.

- 😀 A product with a pre-defined interest rate offers security but involves the risk of missing out on potential higher returns in case of interest rate hikes.

- 😀 The speaker suggests considering longer-term investments (10-15 years) for better financial products and more significant returns over time.

- 😀 For long-term wealth building, variable income products (such as stocks and real estate funds) can turn an investment of R$ 50,000 into R$ 1 million over 21 years at a 15% annual return rate.

- 😀 R$ 50,000 invested in the right long-term financial products could yield substantial returns if you have patience and the right strategy, including investing in good stocks and real estate funds.

Q & A

What is the primary focus of the video script?

-The primary focus of the video is discussing different types of financial products, particularly comparing fixed-income investments with high liquidity options like savings accounts or cash-saving tools from Nubank and Banco Inter.

How much would an investment of R$ 50,000 in a pre-fixed income product return after 59 months?

-An investment of R$ 50,000 in a pre-fixed income product would return R$ 94,800 after 59 months, factoring in taxes.

Why is the return from a fixed-income product higher than from savings accounts or cash-saving products like those from Nubank and Banco Inter?

-Fixed-income products generally offer higher returns because they lock the investment for a longer period, which provides a guaranteed rate of return, unlike savings accounts or cash-saving products that offer lower yields and provide high liquidity.

What risk is associated with pre-fixed income products, as mentioned in the video?

-The risk associated with pre-fixed income products is that if interest rates rise higher than expected (e.g., above 15%), other financial products might offer better returns, leaving the fixed-income investment locked in at a lower rate.

Why did the investor choose the pre-fixed income product despite the potential risk of rising interest rates?

-The investor chose the pre-fixed income product because of the certainty of the high return it guarantees over the next 5 years, as opposed to the volatility of other financial products.

What is the difference between a high-liquidity product like savings accounts and fixed-income investments?

-High-liquidity products like savings accounts provide easy access to funds but offer lower returns, whereas fixed-income investments lock the funds for a longer period but provide higher guaranteed returns.

How could R$ 50,000 transform into R$ 1 million according to the video?

-R$ 50,000 could transform into R$ 1 million if invested in variable income products like stocks and real estate funds, assuming an annual return of 15% over a period of approximately 21 years.

What is the significance of investing in variable income for long-term goals?

-Investing in variable income, such as stocks and real estate funds, is suitable for long-term goals like retirement, as it has the potential for higher returns over time, but it requires patience and a long investment horizon.

What recommendation did the speaker give to the investor regarding extending the investment period beyond 5 years?

-The speaker suggested that the investor could consider extending the investment period to 10 or 15 years to access even better investment opportunities, especially those offering higher returns for the long term.

What type of content does the speaker promise in future videos?

-In future videos, the speaker promises to provide insights on the best stocks and real estate funds of the month, offering detailed information for those interested in long-term investing and building wealth.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

TUTORIAL INVESTASI DARI NOL UNTUK PEMULA

Investasi Jenis Apa yang Cocok untuk Kamu? | feat. Mercy Widjaja

Cara Mudah Menentukan Portofolio yang Efisien | Pemilihan Portofolio

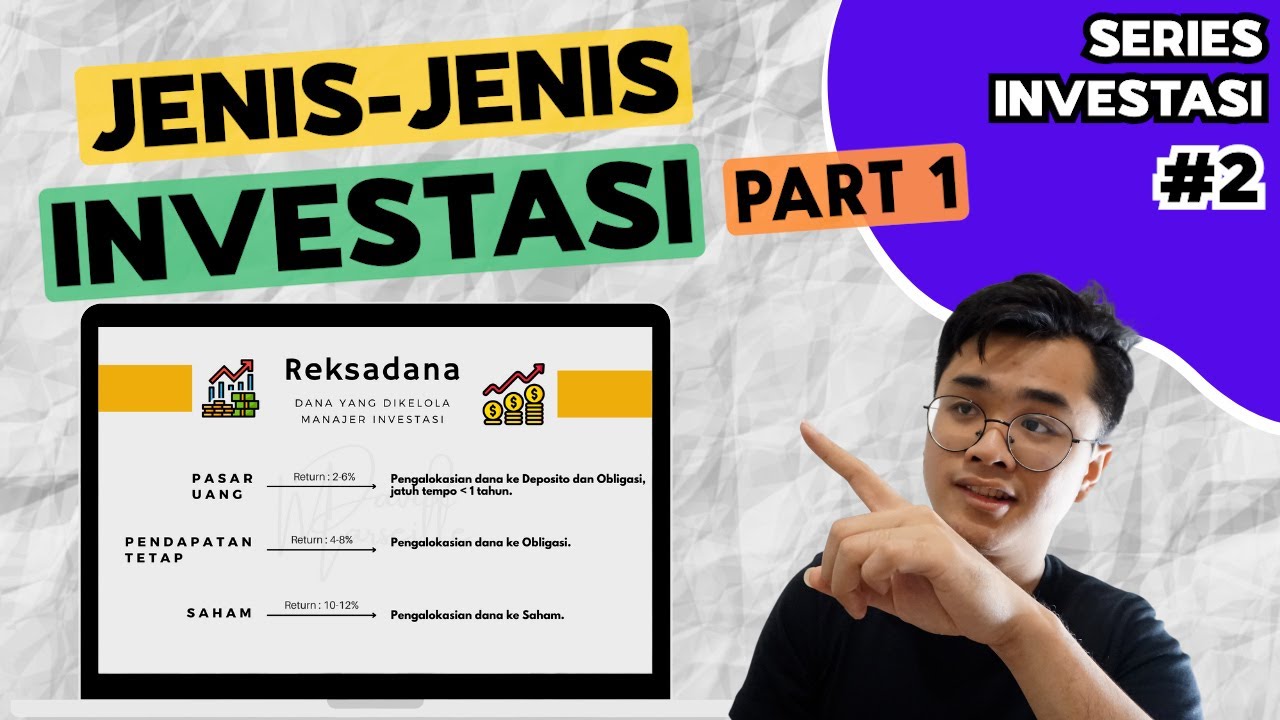

Jenis-Jenis Instrumen Investasi (Investasi Ada Apa Aja Sih?) | Seri Investasi 101 - Episode 2 Part 1

Tahun 2019 Mau Investasi apa?? Emas, Deposito Atau Reksadana? KompasBisnis

AULA COMPLETA para INICIANTES que NÃO SABEM POR ONDE COMEÇAR a INVESTIR

5.0 / 5 (0 votes)