Audit Sampling: Sampling and Non-Sampling Risk CPA Exam

Summary

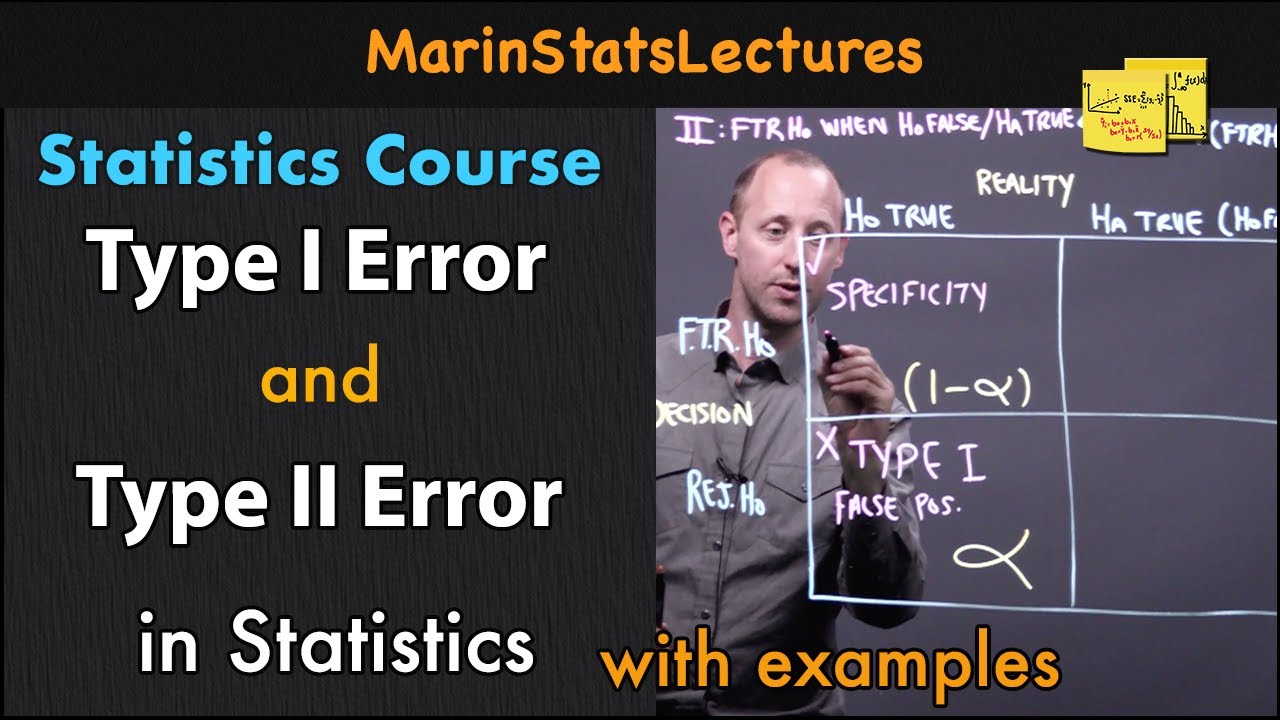

TLDRThe video transcript discusses key concepts in statistical sampling and auditing errors, focusing on Type 1 (alpha) and Type 2 (beta) errors. Type 2 errors occur when a false null hypothesis is accepted, implying financial statements are fairly stated when they are not. Conversely, Type 1 errors happen when a true null hypothesis is rejected, leading to unnecessary work due to an incorrect conclusion about account balances. The speaker emphasizes the importance of understanding statistical versus non-statistical sampling methods for effective auditing and encourages viewers preparing for the CPA exam to study diligently.

Takeaways

- 😀 Sampling is essential in auditing to provide reasonable assurance without reviewing every transaction.

- 📊 Auditors use sampling to draw general conclusions about a population based on a smaller, representative sample.

- 🕒 Conducting a full audit is resource-intensive, so sampling helps save time and money while maintaining reliability.

- 🔍 Two main areas of sampling are 'Test of Controls' for assessing internal controls and 'Substantive Testing' for verifying account balances.

- ⚠️ Sampling risk occurs when the auditor reaches incorrect conclusions due to a non-representative sample.

- ❗ Non-sampling risk involves errors unrelated to the sample selection, such as misinterpreting results or not following procedures.

- 📉 Type 1 Error (Alpha Error) is concluding that internal controls are ineffective when they are actually effective.

- 📈 Type 2 Error (Beta Error) is concluding that internal controls are effective when they are actually ineffective.

- 🧩 Illustrative examples help clarify how Type 1 and Type 2 errors can occur during sampling.

- 🔄 The next session will discuss statistical versus non-statistical sampling methods and their respective applications.

Q & A

What is the primary purpose of sampling in auditing?

-The primary purpose of sampling in auditing is to provide reasonable assurance that financial statements are free of material misstatement, allowing auditors to draw conclusions about a larger population without examining every transaction.

What are the two main types of sampling mentioned in the script?

-The two main types of sampling mentioned are attribute sampling, which tests controls to determine their effectiveness, and variable sampling, which is used for substantive testing to evaluate dollar amounts and account balances.

What is sampling risk?

-Sampling risk is the risk that the auditor reaches an incorrect conclusion due to a sample that is not representative of the population, which can lead to erroneous assessments.

What are Type 1 and Type 2 errors in the context of sampling?

-Type 1 error (alpha error) occurs when the auditor concludes that a control is not effective when it actually is, leading to a false rejection. Type 2 error (beta error) occurs when the auditor concludes that a control is effective when it is not, leading to a false acceptance.

Can you provide an example of how sampling risk might manifest in a classroom setting?

-An example of sampling risk in a classroom setting would be if an auditor samples only students sitting in the front row to determine the percentage of accounting majors in a class of 100, which may not provide a representative sample of the entire population.

What is non-sampling risk?

-Non-sampling risk arises from errors not related to the sample selection process, such as misjudging the quality of evidence or failing to recognize exceptions in the data.

How can auditors manage sampling risk?

-Auditors can manage sampling risk by increasing the sample size, using random selection methods, and understanding population characteristics to avoid bias in selection.

What is the significance of understanding population characteristics in sampling?

-Understanding population characteristics is significant because it helps auditors avoid bias in sample selection, ensuring that the sample is more representative of the entire population.

What are the four scenarios illustrated regarding sampling errors?

-The four scenarios illustrated involve different combinations of effective and ineffective populations and samples, leading to correct conclusions or various types of errors: no error, Type 1 error, and Type 2 error.

What advice is given for those studying for the CPA exam?

-The advice given for those studying for the CPA exam is to study hard and reach out via email if they have any questions, emphasizing the importance of understanding these concepts thoroughly.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

The Population Bag Example

Sampling Risk vs. Nonsampling Risk

How To Identify Type I and Type II Errors In Statistics

Validitas kesimpulan statistik | Statistical conclusion validity

Type 1 and Type 2 errors - Statistics Help

Errors and Power in Hypothesis Testing | Statistics Tutorial #16 | MarinStatsLectures

5.0 / 5 (0 votes)